Asana

The Euros are underway and things are getting heated. Italy is looking fantastic with 3 straight wins and 0 goals against. The Netherlands have been surprising as they are cleaning house in Group C, and Belgium and France are as good as advertised. I’m ready to move past the Group Stages and start getting into the knock-rounds.

The US Open was last week and Jon Rahm earned his first major championship (long overdue). He did it in the best way possible by eagling the 72nd hole and ripping the trophy right out of Louis Oosthuizen’s hands. I feel bad for Oosthuizen who has now placed 2nd in 5 different major championships. Woof.

In other news, Ben Simmons had a rough series and can’t show his face in Philadelphia any more. Red Bull is expanding their lead on Mercedes, and no one watched the French Open this year.

Enough with the introduction, let’s get into it.

But first, this is what I am listening to:

This week we are going to be looking at Asana ($ASAN). As a reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team.

Step 1: Do I understand the business?

Asana is a work management platform that helps teams orchestrate work, from daily tasks to cross-functional strategic initiatives. In short, Asana's mission is to help humanity thrive by enabling the world's teams to work together effortlessly.

One thing to note is that I use Asana in my day-to-day, and it is great for our small team. It’s free for us to use and has been great for everything around project management, onboarding new employees, tracking individual and team tasks, etc.

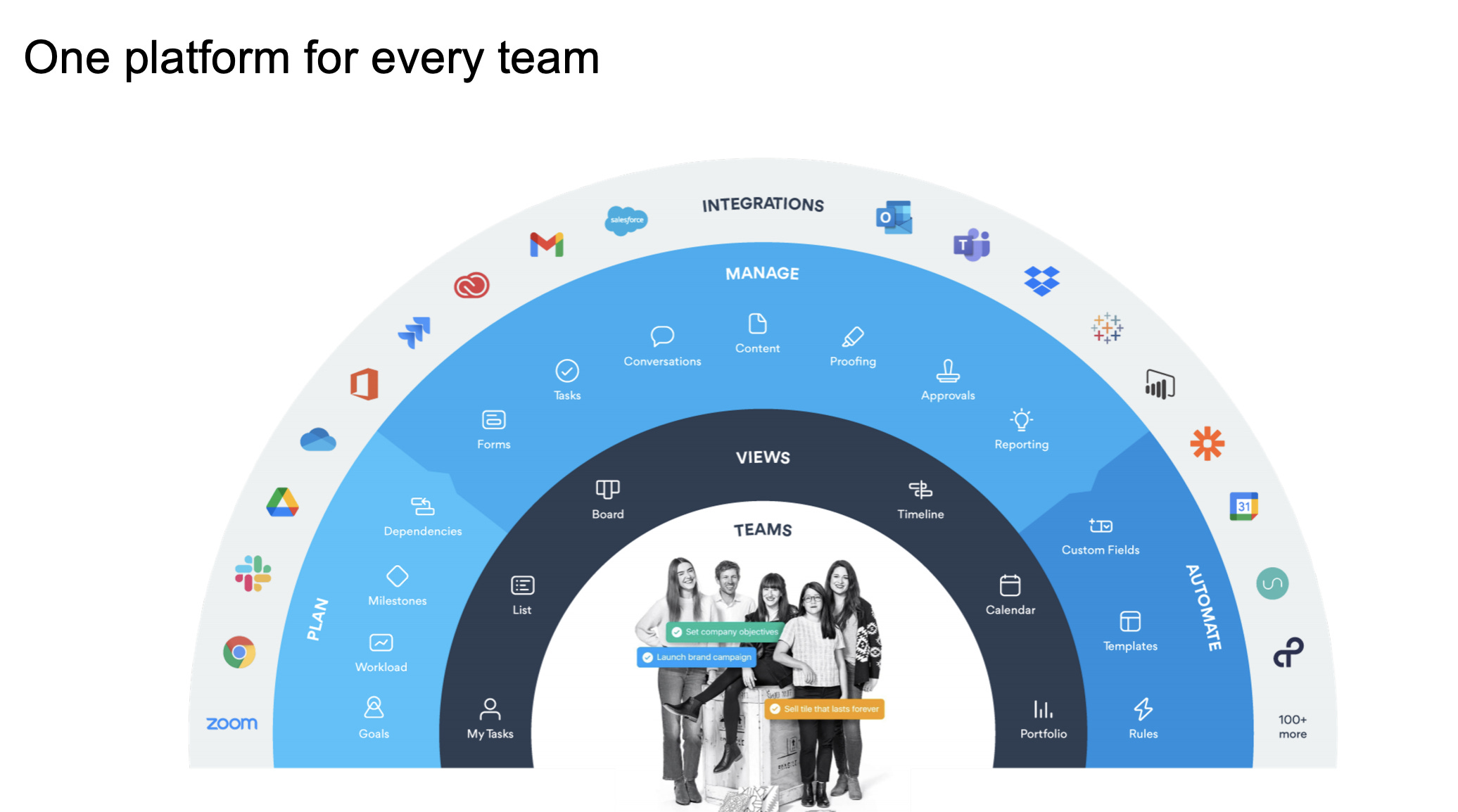

It’s interface is intuitive and has become ‘sticky’ within our organization. They have really integrated themselves well within the software stack:

From a business perspective they are subscription based and have 4-pricing tiers:

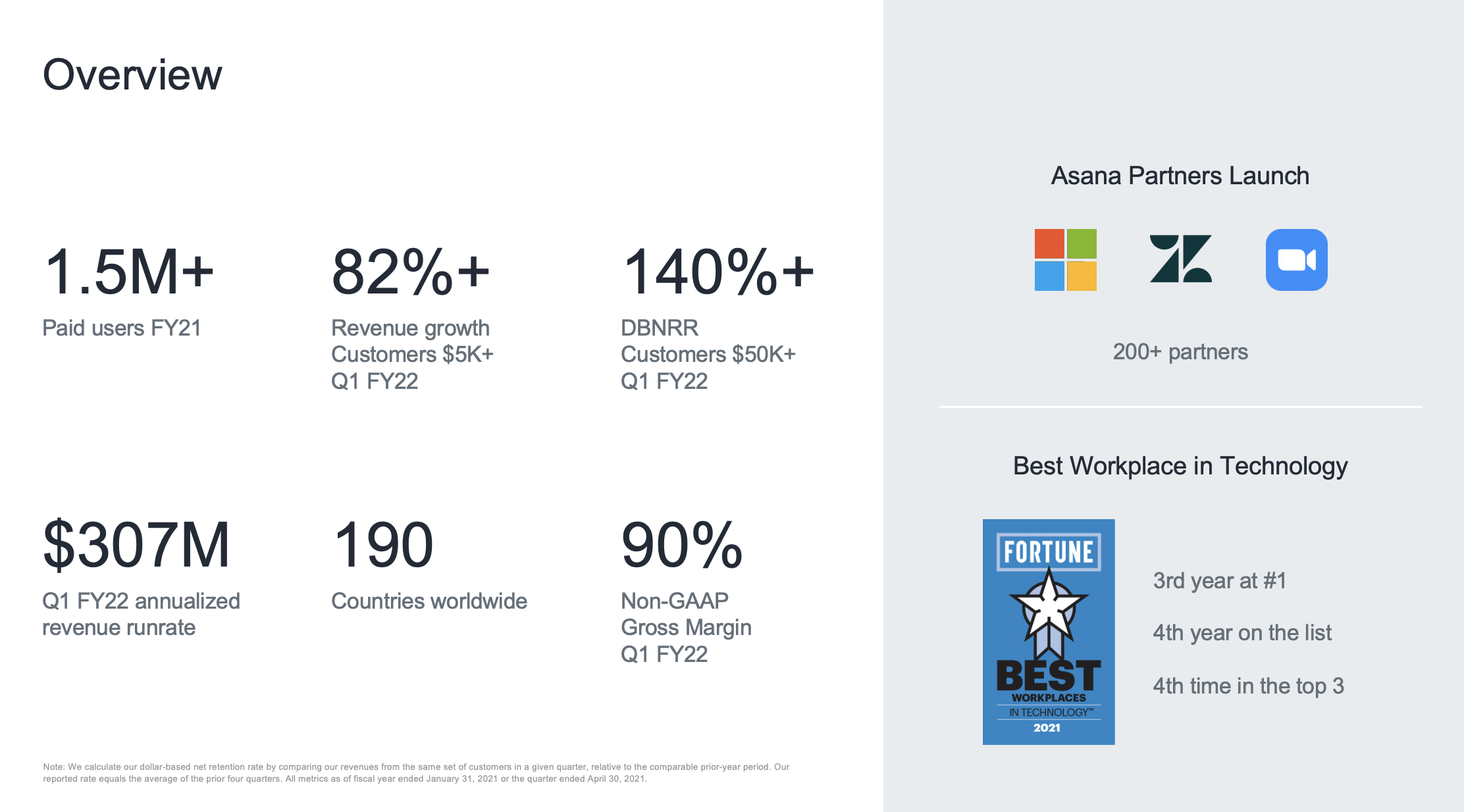

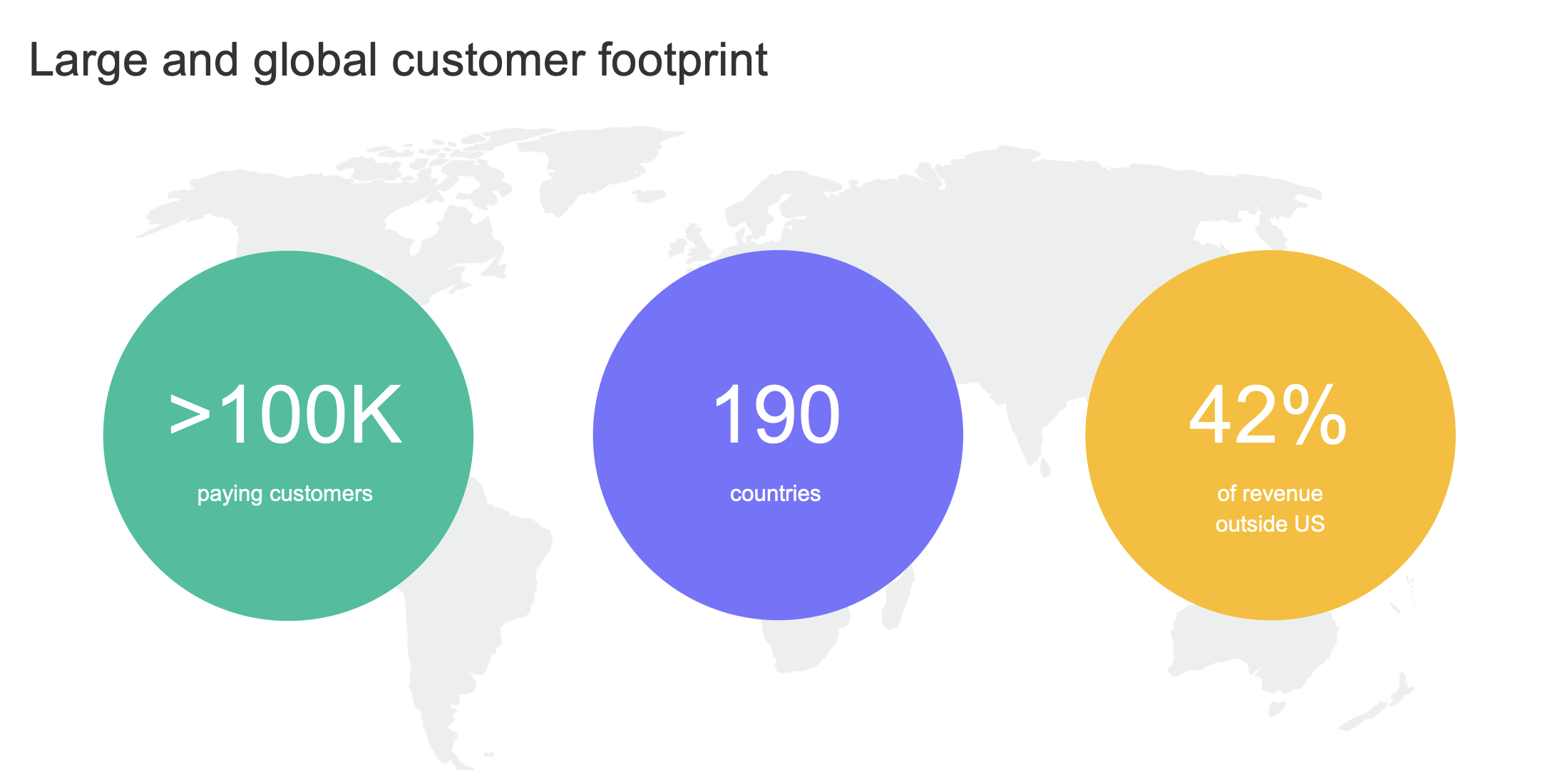

As of April 30 2021, they had over 100,000 paying customers compared to 77,000 as of April, 2020. As for customer concentration risk (they don’t have any), their top 100 customers make up 13% of revenue for April 2021. They currently have 11,272 customer spending over $5,000 (making up 64% of revenue).

Asana has proven their ‘land-and-expand’ strategy works and can continue to generate revenue for them. In 2020, they had 252 customers spending over $50,000 and in 2021, they had 485 customers spending over $50,000 (almost 100% growth within 12 months!).

Being able to leverage existing customers as a meaning full revenue generator helps in two areas - 1) top line growth and 2) helps keep costs down for Sales and Marketing. Asana’s ability to expand within customers is basically adding fuel to the fire for a fast growing company.

They had Dollar-Based Net Retention Rate (DBNRR) of 115% in 2021 for all customers ( this is fantastic). And most importantly, they are seeing even better DBNRR within their top customer accounts: for customers spending over $5,000 with Asana had a DBNRR of 123%, and for customers spending over $50,000 with Asana had a DBNRR over 140%.

Verdict: I like the business and I like the tool.

Step 2: Moat and Future Growth/Catalysts

Asana has a moat. They are best in breed in terms of Brand, Reputation, and Workplace Culture. They will continue to add customers and to develop their product, but I am not sure their moat is expanding or how deep the waters are.

One thing to note is tis moat will be costly to maintain. Currently, Asana’s two biggest operating expenses are R&D, and Sales and Marketing. And for the foreseeable future, Asana will need to spend huge amounts of money to keep up with Product Development and fight against competition.

The Project Collaboration Software space is full of competitors. There is Monday.com ($MNDY) which just went public and has a ton of momentum. They face competition from Trello, Smarsheets ($SMAR), etc, and even face ancillary competition from products like Slack or Microsoft Teams. Get to a full view of the landscape check it out here.

Here is how Asana’s moat currently sits (see below).

I like that they are focused outside of the US. Being global gives them a physical moat, and it also gives them a much larger market to target.

Emerging markets may be their ‘blue ocean’ while other companies fight over more developed markets. Just within the last quarter, they expanded with four new languages - Traditional Chinese, Russian, Dutch, and Polish, with three more languages coming soon.

Verdict: They have a moat, but I’m not sure how strong it is or how they continue to differentiate themselves against TOUGH competition.

Step 3: Management

Dustin Moskovitz is the CEO and Co-Founder. As mentioned in my last post, I like management team’s who have skin in the game and who have had success in their pasts’. Moskovitz meets that description perfectly. Moskovitz was a co-founder of Facebook and operated as FB’s CTO and VP of Engineering.

He has a ton of skin in the game, and he has recently been buying $ASAN hand over fist. This a huge positive for me.

Moskovitz could literally be doing anything and instead of riding off into the sunset, he is deciding to spend his time growing Asana. He clearly believes in it and he’s even buying more of it!

Verdict: I am a fan

Step 4: Valuation

High-level tradition metrics:

Market Cap: $9.46B

EV: $9.68B

EV / Revenue: 26.77x

Price / Sales: 36.91x

NTM Revenue: 361.8x

Gross PM: 88%

$ASAN is trading at a very similar valuation to $SMAR and at a discount to $MNDY. If we compare $ASAN to $TEAM they have a similar EV / Revenue, but $TEAM is a significantly more developed company and probably the better bet over the next 5 years.

$ASAN is only a ~$10B company, but I’d like it a lot more if it were still in the mid-low single digits. At a +57% revenue growth rate, $ASAN deserves the premium, but I’d probably wait to see how it performs over the next few quarters as 1) competition increases and 2) the growth from COVID19 slows down.

Can $ASAN keep up the revenue growth at scale as end-users come back into the office? I am not saying existing customers are going to churn, but what I am saying is that new large ‘logos’ will become harder to find.

I like $ASAN ~$30. At $30, there is a slight margin of safety for investors and gives the management team some ‘margin’ for error when it comes to executing at scale.

Verdict: It’s rich, but not egregiously so. It’s definitely worth a look if you want exposure to the B2B Software space and a fast growing company.

The Rookie Quick Fire Challenge - LINK HERE

Score 39.5 / 81

Overall Verdict: I’m a big fan of Asana…at the right price. It’s a different bet at $10B vs $5B.