California Water Service Group Holding

California Water Service Group Holding

$CWT, where oh where will all of the water go?

Water. Bruce Lee knew what water was all about:

How is California doing?

This is an aerial photo of Lake Oroville which is the California’s second-largest reservoir and a crucial source of water supply for the state's farm and city water users alike. Lake Oroville is suppose to supply nearly 27 million people and 750,000 acres of farmland with water, but this year it won’t be able to do that.

We had water…and it’s gone.

We are getting drier and drier every year. The wet season is shorter and summers are longer. Everyday there are headlines like:

Valley farmers might face harshest ever water restrictions due to drought

Water crisis reaches boiling point on Oregon-California line

Thousands of Central Valley farmers may lose access to surface water amid worsening drought

Water shortages: Why some Californians are running out in 2021 and others aren’t

But why I am talking about water shortages here? Great question - I want to better understand how publicly traded water companies work. And specifically, I want to better understand how California Water Service Group Holding $CWT works.

But first, here is my jam for the week

Let’s get into it.

As a reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team.

Step 1: Do I understand the business?

California Water Service Group $CWT is a holding company with six operating subsidiaries. They mainly operate in California, New Mexico, Washington state, and Hawaii.

$CWT and it’s subsidiaries provide utility services to ~2 million people. $CWT mainly focuses on the production, purchase, storage, treatment, testing, distribution and sale of water for domestic, industrial, public and irrigation uses, and for fire protection.

In specific areas they provide wastewater collection and treatment services, including treatment which allows water recycling.

They also provide non-regulated water-related services (i.e. water system operation, billing and meter reading services) under agreements with municipalities and other private companies.

Broken down by region, $CWT makes most of it’s revenue from their California operations which supplies water services to 492,600 costumers as of 2020 (90.7% of $CWT’s customer connections).

In short, $CWT makes money by “providing regulated water and wastewater services at tariff-rates authorized by the Commissions in the states in which they operate and non-regulated water and wastewater services at rates authorized by contracts with government agencies. Revenue from contracts with customers reflects amounts billed for the volume of consumption at authorized per unit rates, for a service charge, and for other authorized charges.”

That is a mouthful but one red flag that jumps out to me is that “rates authorized by contracts with government agencies” signifies to me that $CWT pricing power is limited and thus revenue growth is capped.

$CWT recognizes this as a risk as well, and in their own words states “The Commissions have plenary powers setting both rates and operating standards. As such, the Commissions’ decisions significantly impact the Company’s revenues, earnings, and cash flows.”

There are several other ‘things’ that I don’t love about the $CWT business: 1) continual need for high CapEx+COGS, 2) acquisition is the main vehicle for growth (aka limited organic growth and low optionality for the business), and 3) exposure to macro level weather changes (i.e. droughts, floods, fires) that could impact every operational level of the business.

Verdict: Fail - I get the business model but nothing excited me about it.

Step 2: Moat and Future Growth/Catalysts

Let’s address $CWT’s moat - it is solid.

I don’t see $CWT moat shrinking. $CWT’s moat is built on two principles 1) it’s unique position as a utility provider, and 2) it’s relationship with the government (decade long contracts for the areas they operate in).

And they even have the potential to expand their moat as they look to enter new markets.

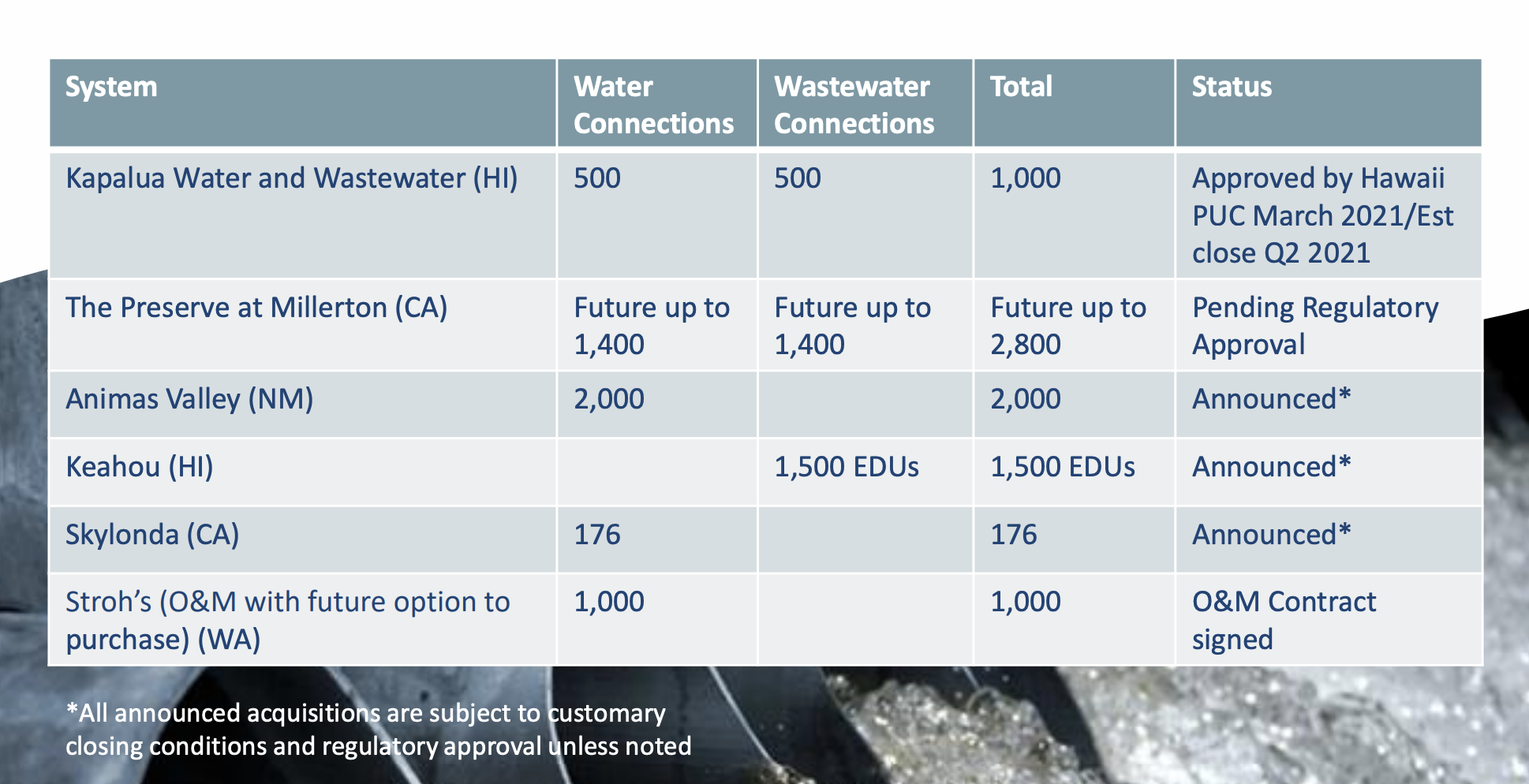

Here are just a few of their acquisitions from their last 2021 first Quarter report:

Here is how they view their position growth moving forward “we intend to continue exploring opportunities to expand our regulated and non-regulated water and wastewater activities, particularly in the western United States. The opportunities could include system acquisitions, lease arrangements similar to the City of Hawthorne and City of Commerce contracts, full service system operation and maintenance agreements, meter reading, billing contracts and other utility-related services.”

$CWT’s growth will come at a cost and most likely a premium price.

$CWT has limited optionality (i.e. they can’t release a new product line over night) and are limited in revenue growth by rates.

In terms of competition, $CWT doesn’t really have any. It’s fairly difficult for startups to disrupt the water utility business, and “Our principal operations are regulated by the Commission of each state. Under state laws, no privately owned public utility may compete within any service territory that we already serve without first obtaining a certificate of public convenience and necessity from the applicable Commission. Issuance of such a certificate would only be made upon finding that our service is deficient. To management’s knowledge, no application to provide service to an area served by us has been made.”

That is an amazing quote. You should read it again.

In short, future growth is limited and probably going to be expensive, but $CWT has the luxury of NO competition and extremely long contracts for the areas/communities they operate in.

This means that as long as $CWT can manage operational costs, execute favorable contracts and rates, move into more strategically impactful regions, and manage their macro-risks, they’ll probably be at least mediocre.

Verdict: Meh - The Moat is great, but growth is whatever.

Step 3: Management

This is my own bias, but whenever I hear about public utility companies management team’s, I think of PG&E and how corrupt their leadership has been.

I looked into $CWT and the incentives for leadership don’t seem out of line with shareholders interest. With that said, I am not a corporate governance expert and you should due your own due diligence here.

Not necessarily related to management, but $CWT is tightly associated with Unions and I am NOT a fan of those. To be clear, I like unions and support workers joining them, but they aren’t my favorite as an investor.

Management is fairly boring, but boring can be good. I didn’t see any scandals and they seems to be investing heavily in ESG.

Verdict: I got bored reading their bios.

Step 4: Valuation

The fun part. How do you value $CWT? Let’s start with high-level metrics.

Share Price: $62.31

Market Cap: ~$3.2B

EV: ~$4.3B

Shares Outstanding: ~50.84MM

Gross PM: ~52%

NTM EV / Revenue: 5.23x

NTM EV / EBIT: 24.89x

$CWT has been free cash flow negative for the last 5 years. Some rough math, if we assume a revenue growth rate of 7% (their average over the last 5 years) for the next 10 years, apply a ~5% discount rate, I get a fair value of around $55.

And then add on my 10% margin of safety and I get ~$50 per share.

I’m sure someone out there could do a more accurate valuation model, but that doesn’t really matter to me. What matters to me is understanding if a company is trading at a premium or not, AND if that premium is worth paying for.

$CWT is trading at a premium. It makes sense. It’s going to grow (slowly), it sells a product we NEED everyday, it pays a solid dividend, and has no competition.

Verdict: Fair - Pass

The Rookie Quick Fire Challenge - LINK HERE

Score 46.5 / 81

Overall Verdict: Interested, but in my opinion it’s not worth the premium price. This isn’t a tech company where the price you pay is secondary to the company’s growth prospects. Valuation matters more with companies like $CWT and at this price, I’m not sure you beat the S&P 500 over the next 5 years. I’d rather have my money in $SPY than $CWT at this price.