Earnings Season Q1'23

The Rookie Lineup

Disclaimer: This is NOT investment and/or financial advice and shouldn’t be used as such. This is for entertainment purposes only.

Q1’23 Earning Season is underway and this one is more important. Its important for a few reason, but mainly, this will be the first chance to see if we’re through the pain of 2022.

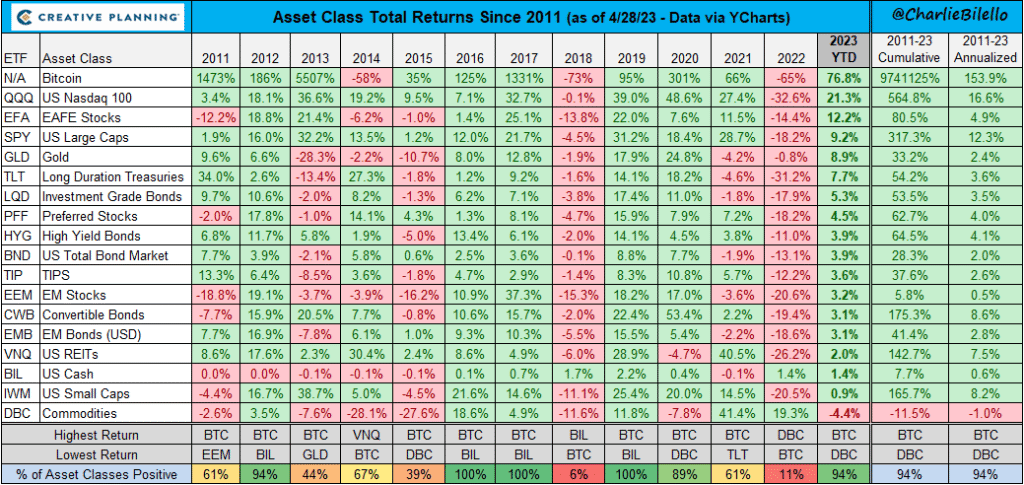

2022 was a dark. Everything got murdered - see below for proof. Source: The Week in Charts (5/2/23) by Charlie Bilello

And that’s what makes this earnings season so important. It’s our first opportunity for management and leadership teams to - hopefully - tell us that we’re through the dark forest and into happier pastures.

Atlassian TEAM 0.00%↑

The Good

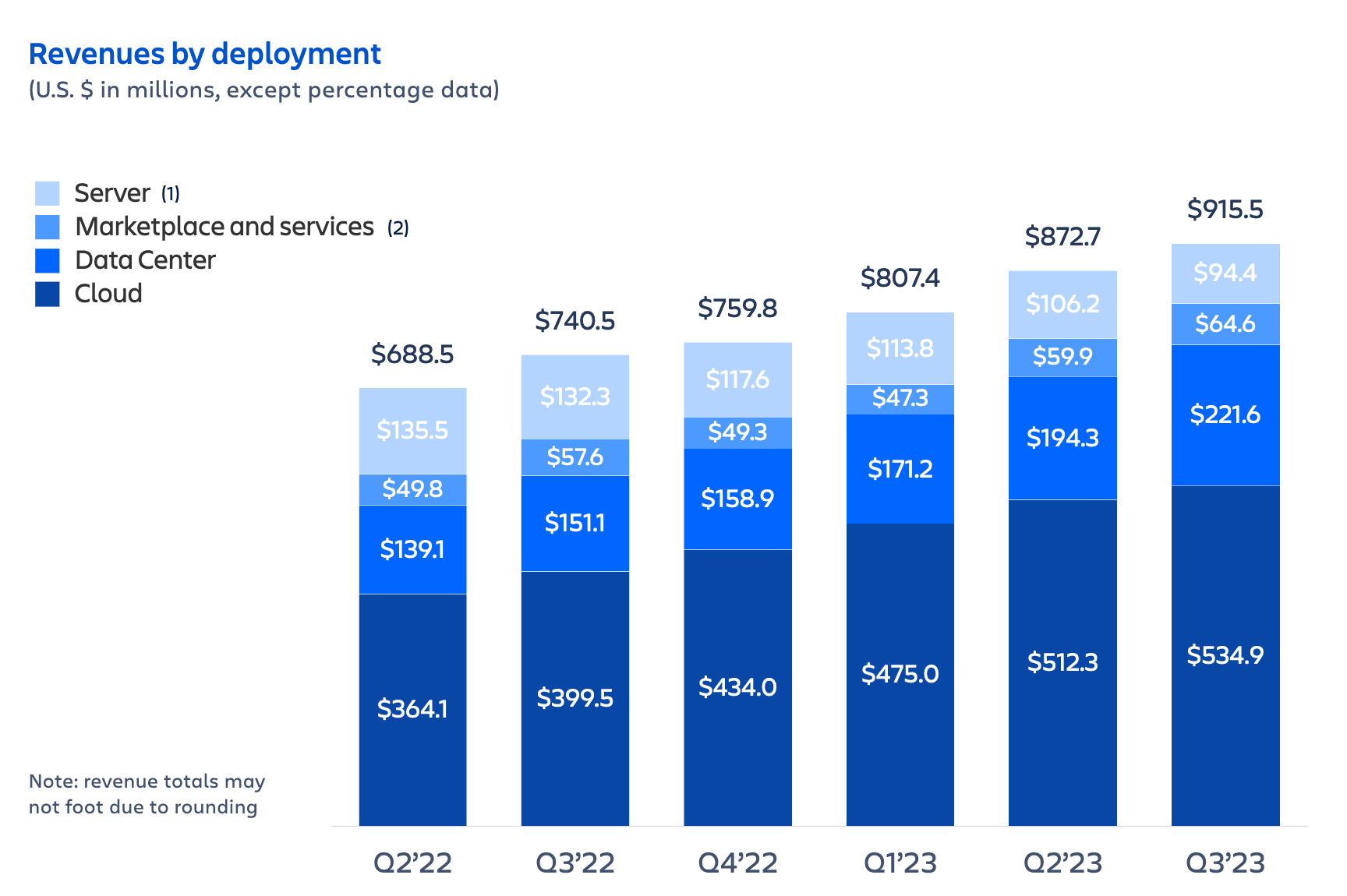

$915M Revenue (+24% YoY) vs $901M consensus (2% beat)

$761M Subscription Revenue (+37%) YoY

82% Gross Margin (down from 84% last quarter) // 38% FCF Margin

Continued penetration into extremely large customers: Atlassian announced the general availability of 50,000-user instances for Confluence Cloud, enabling larger organizations to unlock the benefits of cloud and scale their usage of our products

The Bad

$910M next Q guidance vs $917M consensus (1% miss)

53% increase in operating expenses! Spending on R&D, and Marketing and Sales, is outpacing revenue growth over the last 12 months. This will need to be watched/fixed.

Stock-Based Compensation was 28% of revenue - ugh. This is a true cost to the business and impacting results.

Important Quotes from Leadership

CEO “Trends in the quarter were largely consistent with the H1 23. Cloud revenue growth was driven by existing customers & migration activity, while impacted by macro headwinds. Data Center revenue benefitted from strong renewal”

CEO “The moderating growth rate of cloud revenue continues to be impacted by worsening macroeconomic headwinds on paid seat expansion from existing customers, free-to-paid conversions, and modest seat count reductions in some customers that have announced layoffs”

Summary

The market puked at this report. TEAM 0.00%↑ was down 13% on the announcement and ended down on the week. I'm not sure the report deserved such a thrashing, and it was 'ok' for this macro-environment - not thesis breaking.

Things I’d like to see next quarter:

Continue +25% revenue growth, lower operating expenses, slower SBC, continue FCF growth.

Confluent CFLT 0.00%↑

The Good

$174M Revenue (+38% YoY) vs $167M consensus (4% beat)

$74M Confluent Cloud Revenue (+89% YoY)

$640M ARR (+41%)

>130% DBNR at 67% Gross Margins

1,075 customers with $100,000 or greater in ARR, up 34% year over year

The Bad

(48%) FCF Margin

Important Quotes from Leadership

CEO “Traditional on-premise open source business models offer a premium product, better features for more money. As a result, they typically are able to capture only a fraction of the open source users as paying customers. The cloud product, however, isn't just replacing the free software. It's also replacing the expensive infrastructure and people costs. This is driving a general mindset shift among software engineers and IT departments, who are increasingly looking for managed services first, trying to avoid ongoing operations wherever possible.”

Summary

Confluent showed and provided they are a mission critical software. Leadership demonstrated they can execute in a turbulent environment.

The question now is can they keep this performance up year over year, and drive positive FCF.

Datadog DDOG 0.00%↑

The Good

$482M Revenue (+33% YoY -3% beat)

Added ~$50M Net New ARR, down from ~$130M Q4’22 and ~$150M Q1 '22

>130% DBNR at 79% Gross Margins

24% FCF Margin

Strong growth of larger customers, with about 2,910 $100k+ ARR customers, up from about 2,250 a year ago

81% of customers were using 2 or more products, in line with last year. 43% of customers were using 4 or more products, up from 35% a year ago. And 19% of our customers were using 6 or more products, up from 12% last year

CEO “We achieved FedRAMP moderate authorization and have since landed a number of government agencies as customer”

The Bad

BIG outage this quarter reduced revenue by $5M

On a GAAP basis, Datadog is not yet profitable.

Important Quotes from Leadership

CEO “Now let me speak to our longer-term outlook and my thoughts on 2023. Although we are seeing customers be more cautious with their cloud usage expansion in the near term, we see no change to the long-term trends towards digital transformation and cloud migration. We think it's healthy for customers to optimize, and we believe that the ability to correct course and continually align the nature and scale of their applications with their business needs is one of the key benefits of cloud transformation.”

CEO “Regardless of near-term macro pressure, we believe it is still early days, and we expect that companies worldwide will continue to grow their next-gen IT footprint to deliver value to their customers”

Summary

Solid and good quarter. The outage hurt, but they exceed expectations anyway. DDOG 0.00%↑ proved why they are so highly valued.

Shopify SHOP 0.00%↑

The Good

Shopify sold its Logistics infrastructure to Flexport Good, I am glad Shopify Leadership was brave enough to recognize this was not worth the money

Total revenue increased 25% to $1.5 billion compared to the prior year

Merchant Solutions revenue increased 31% to $1.1 billion compared to the prior year

Free Cash Flow was $86 million or 6% of revenues, compared with negative free cash flow of $41 million or 3% of revenues in the first quarter of last year.

Monthly Recurring Revenue as of March 31, 2023 increased 10% to $116 million compared to the prior year. Gross Marins at 48% (53% last year)

The Bad

Shopify sold its Logistics infrastructure to Flexport. Bad, think of all the wasted resources, time, attention, and money that went into this over the last 3 years.

Summary

I still don’t fully trust Shopify’s leadership, but this quarter was a step in the right direction.

I want to see FCF stay positive (and grow), and Gross Margins (change directions see above) and business efficiencies improve this year. Jeff Hoffmeister, CFO, as Tupac would say “all eyez on you”.

Here’s what we have left on the calendar:

TEAM - Reported

CFLT - Reported

DDOG - Reported

SHOP - Reported

U - May 10th

DIS - May 10th

ZS - May 24th

COST - May 25th

HD - May 16th