Liberated Syndication Inc

Liberated Syndication Inc

$LYSN, will podcasts continue to eat the world?

May was a great month for sports. Monaco was a fantastic race and this season has been the most intense battle for the Constructor Cup in the last 5-6 years. Red Bull (1st) is 1 point ahead of Mercedes in the standing, and Sir Lewis Hamilton is starting to show weakness in his armor.

Baseball is in full swing. The SF Giants and Oakland As are killing it this season, and are fighting for their respective NL / AL West Division titles - life is good when the Bay Area' sports teams are winning.

Basketball playoffs have started (Phoenix is a great story). The Warriors have been knocked out, but it was an amazing last 2 months watching Steph Curry put up 40 pts night-in, and night-out. What a Stud. Warriors will be a problem for the league next year.

I’ve been listening to a shit-ton of podcasts over the last 3-4 years, and I am addicted. Podcasts have become invaluable in my life. Not only do podcasts offer entertainment and educational content, but there is an intimacy with the hosts + guests of the podcasts that only comes from this form of media.

For this reason, I’ve decided to delve into Liberated Syndication Inc ($LYSN) for this week’s post.

Before we jump in, this is what I am listening to:

Reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team.

Step 1: Do I understand the business?

Before we jump into $LYSN, let’s understand the podcast market. According to BusinessWire, the podcast market is suppose to reach $41.6 Billion by 2026 with a 24.6% CAGR between 2020 - 2026.

It’s clear the podcast industry is booming and will continue to do so.

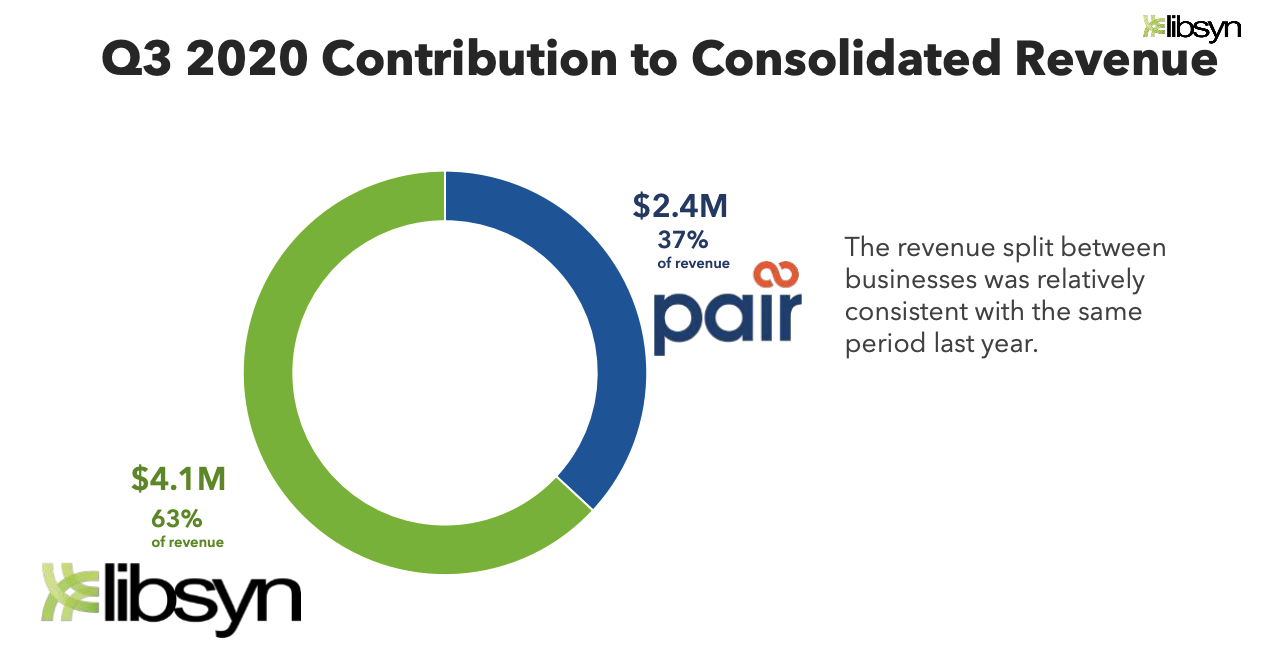

$LYSN may be well-positioned to take advantage of this boom and could be the classic ‘picks and shovels’ play. In short, Liberated Syndicate operates two verticals, Libsyn and Pair. Libsyn, “is a podcast service provider offering hosting and distribution tools which include storage, bandwidth, RSS creation, distribution, and statistics tracking. Podcast producers can choose from a variety of hosting plan levels based on the requirements for their podcast” (10Q-Q3-2020). Pair Networks is an “Internet hosting company”. Here is a breakdown of how each vertical contributes to revenue:

Libsyn had a 18% CAGR between 2016 - 2019 and Pair experienced a 3.5% CAGR between 2018-2019. These aren’t huge numbers but they are growing.

The pandemic should’ve helped these numbers, but it didn’t - something isn’t working. This begs the question for future growth of how expensive new Customer Acquisition will be?

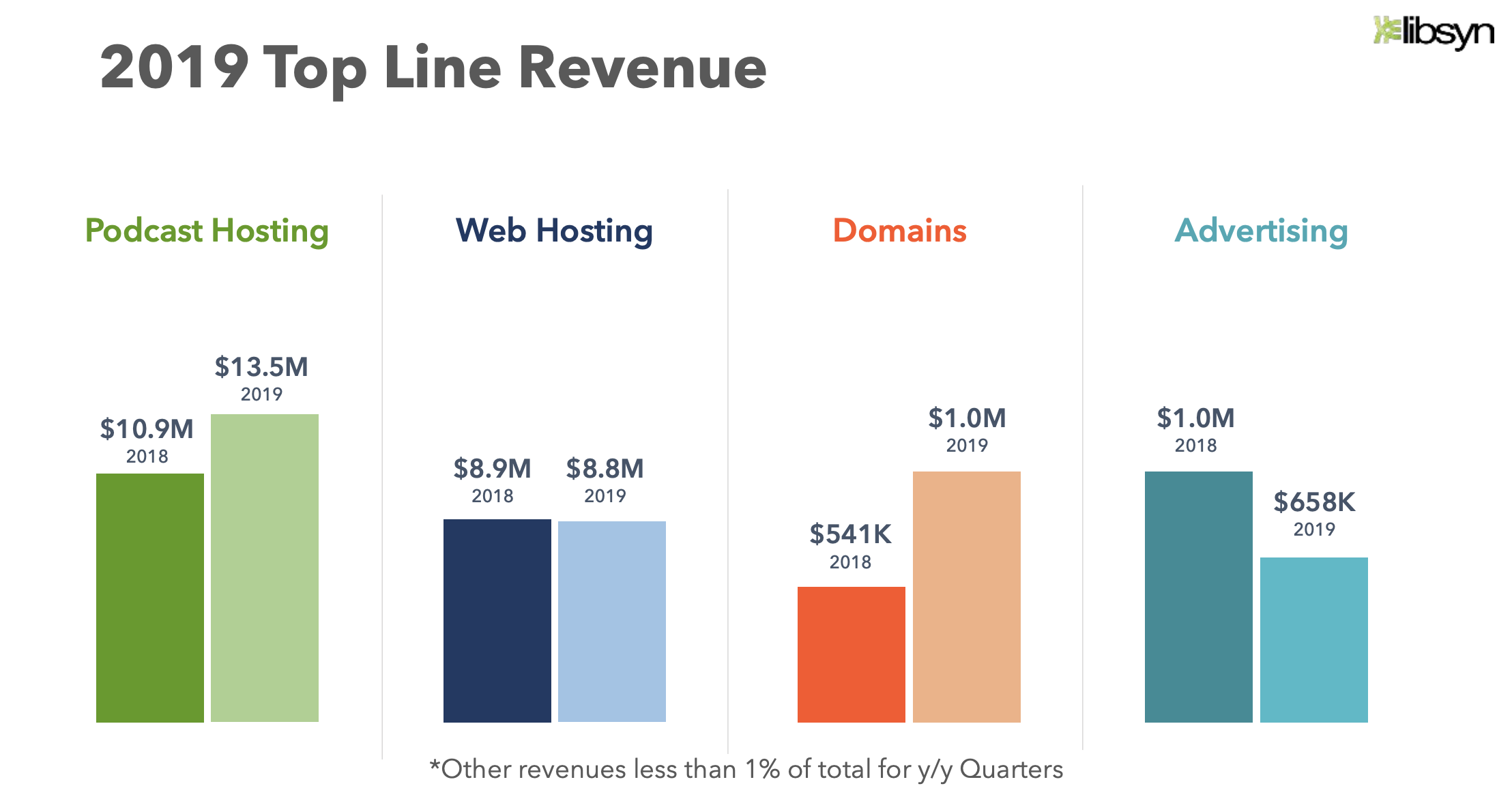

Based on 2019 numbers (full 2020 numbers have yet to come out or I wasn’t able to find the SEC filing), it looks like Podcast Hosting is their best vertical and I’m surprised that Advertising is trending in the wrong direction.

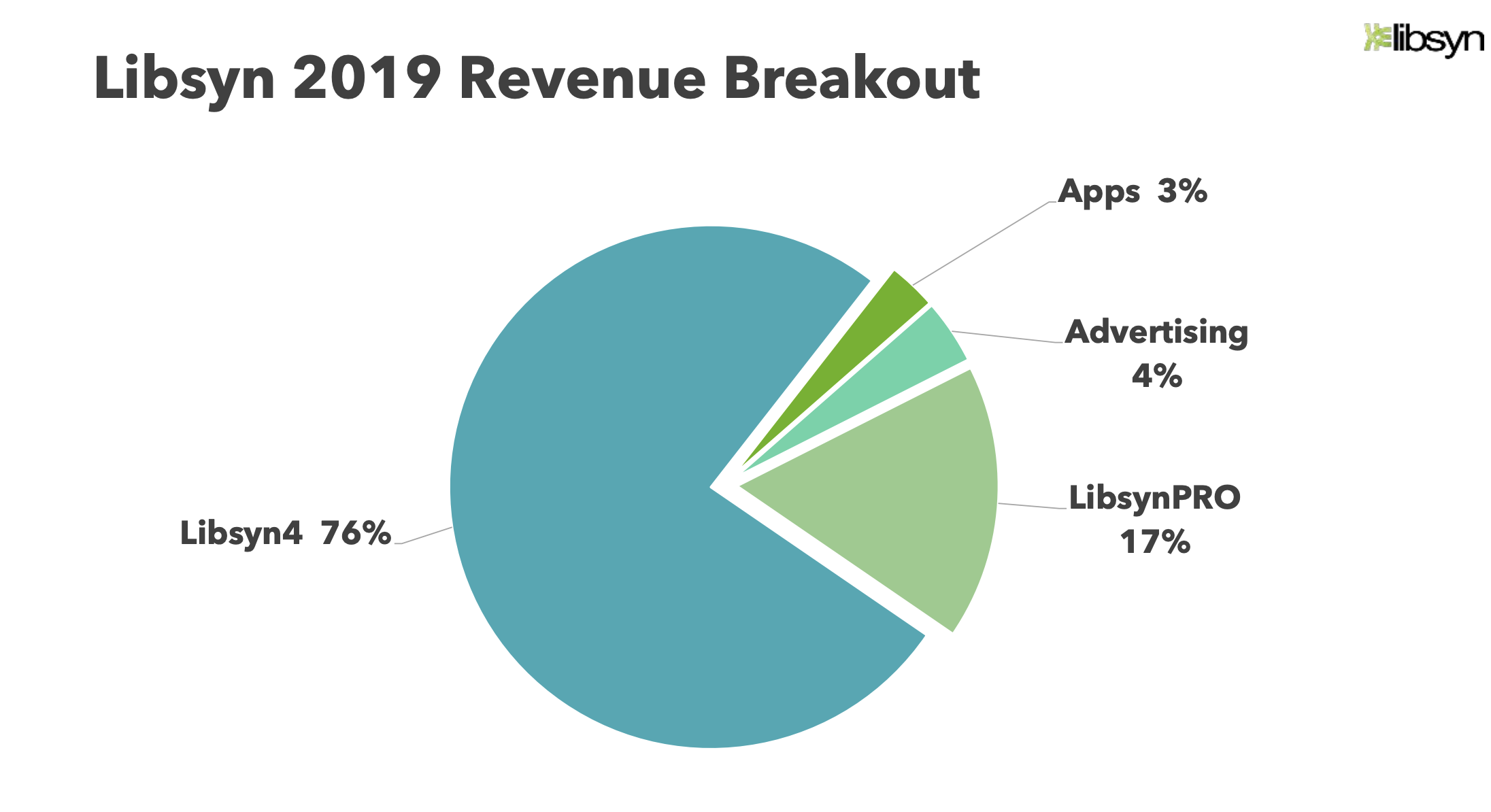

I like Liberated’s business model. They are a SaaS platform where revenues come from Monthly Fees and customer expansion. They have different pricing models depending on customer need, and 17% of Libsyn revenue comes from their LibsynPro Tier. I’d like to see this piece of the pie continue to grow.

There is low customer-concentration risk as they host 75,000 podcasts around the world with a churn rate of appreciably under 3%. One metric I’d like to better understand is what % of revenue is made up by the Top 20 customers? (This would validate the low customer-concentration risk).

I’d also like visibility into their Net Revenue Retention (NRR) to better understand the rate they are expanding within existing customers, minimizing churn, and adding new customers.

In Q3, 2020 Libsyn partnered with Amazon Music / Audible to expand it’s reach within the Podcast Market, and they partnered with Gaana who is India’s top music streaming service and top 5 globally. These partnerships should help expand Liberated’s TAM and distribution channels.

Along this same theme, Liberated recently acquired Glow which is a Podcast Monetization platform that, “enables podcasters to build membership programs and

generate listener-supported revenue”. It will be interesting to watch how Libsyn incorporates Glow into their product offering, and if it really moves the needle for top line growth.

Verdict: I like the business, but don’t love it.

Step 2: Moat and Future Growth/Catalysts

Liberated’s moat is fine. Customer’s don’t churn once on platform, but I’m not sure how Liberated continues to differentiate itself against competition or other podcast hosting platforms.

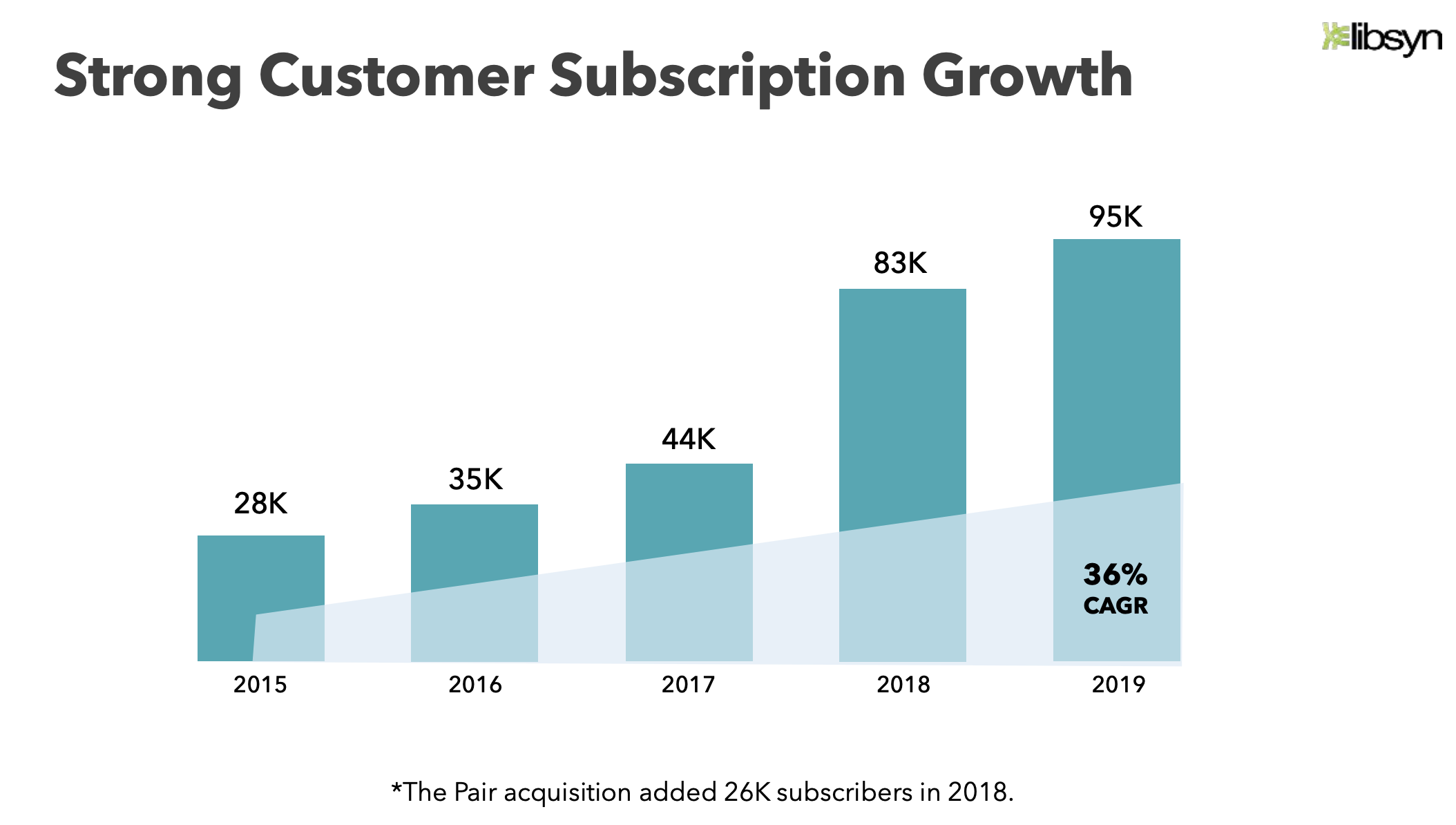

With that said, they have proven to have strong customer subscription growth. This is great, but it does seem that huge growth will only come through acquisitions* (Big * on the image below). This is a tough game to play and costs a shit-ton-of-money.

In addition to this, their 4 pillars for Growth and Valuation Creation are snoozers:

Build on Trust Reputation

Increase Addressable Market (aka more acquisitions)

Leverage Technology Platform (aka upsells and expansions)

Create Value Across Platforms (increase customer LTV in the Liberated ecosystem)

These pillars don’t inspire me or get me that excited as an investor / business owner. Liberated is trying to become the one-stop-shop for everything Podcast / Audio creation. This is a strong value proposition.

One thought I’ve had is that as Liberated continues to grow and acquire new businesses this makes them an attractive acquisition target for the likes of Spotify, Apple, or any other major player in the creator platform space.

There is a near-time catalyst that was written about by Pounding the Rock Investing and this could be a reason to hold the stock - this is obviously an arbitrage-type play and not within the Rookie Checklist system, but an interesting thesis nonetheless.

Verdict: They have a moat (kind of), but not sure of it’s long-term durability and if Liberated has huge pricing power.

Step 3: Management

Back in August 2020, Chris Spencer, stepped down as CEO. Since them, Laurie Sims has been running the show as COO and she owns ~4.3% of the company.

One concern I have is that they don’t highlight their management, company values, or company mission well on the website. It is either hidden, non-existent, or difficult to find.

I generally like seeing management teams presented on the website. I like seeing company values and inspiring mission statements. Liberated does none of this, and this makes me question who is running the company.

There is no news of a new CEO yet.

Legal issues are also never a good sign.

Verdict: Fail.

Step 4: Valuation

High-Level Numbers

LTM EV / Revenue: ~4x

LTM EV / EBIT: 19.18x

LTM P / Sales: 4.76x

LTM GPM: 87%

Levered Free Cash Flow Margin %: 35% (stable YOY)

$LSYN has very little debt, they have cash on the balance sheet, they generate FCF, and overall have a good balance sheet / income statement. The COGS have gone up and I assume their operating expenses will continue to increase as they search for growth.

They aren’t egregiously overvalued or undervalued. I don’t see a huge ‘margin of safety’ at $4 price / share.

I didn’t even bother with a DCF due to the poor Management Scoring.

With that said, the valuation for $LSYN isn’t black or white. I think if $LSYN had a great management team then $4 price/share would be a good investment, but with it’s lack of leadership, and required focus on legal issues, it’s going to be rough future.

Do I really want to be in-bed with these people? Probably not.

Does $LSYN beat the SP 500 over the next 2-3 years? Probably not.

Verdict: Fail.

The Rookie Quick Fire Challenge - LINK HERE

Score 34 / 81

Overall Verdict: I like the business, but management is a problem. Pass.