Red is my favorite color

Jams first. Music is like food. You are what you eat, and you are what you listen to.

It’s been a while. Life has been hectic and I lost steam. But I am back. I plan to pick up where I left off with around 1-2 posts per month.

What a way to finish the week. (source: finviz.com)

Is this a sign of a ‘greener’ pastures and that tough times are behind us? I’m skeptical. Nick Maggiulli had a wonderful blog post, Rallies to the Bottom, where he describe this exact phenom:

In the great financial crisis from 2007-2009, the DOW rallied 3 TIMES at 11%, 18%, and 20%, and still continued to destroy capital. Lower lows and lower highs.

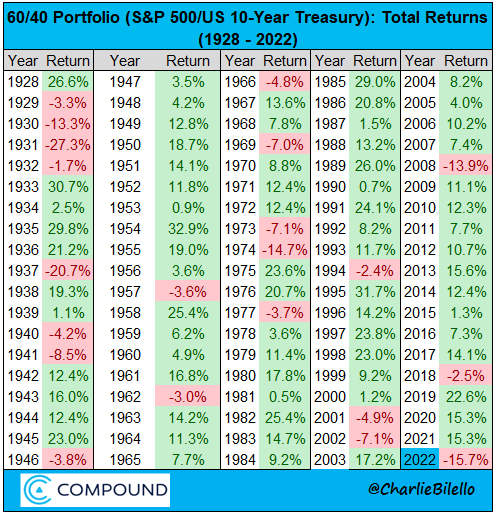

2022 has been a historically bad year for investors, and there is no place to hide.

Charlie Bilello highlighted this beautifully, “A 60/40 portfolio of the S&P 500 and 10-Year Treasury Bond is down 15.7% year-to-date, on pace for its worst year since 1937.”

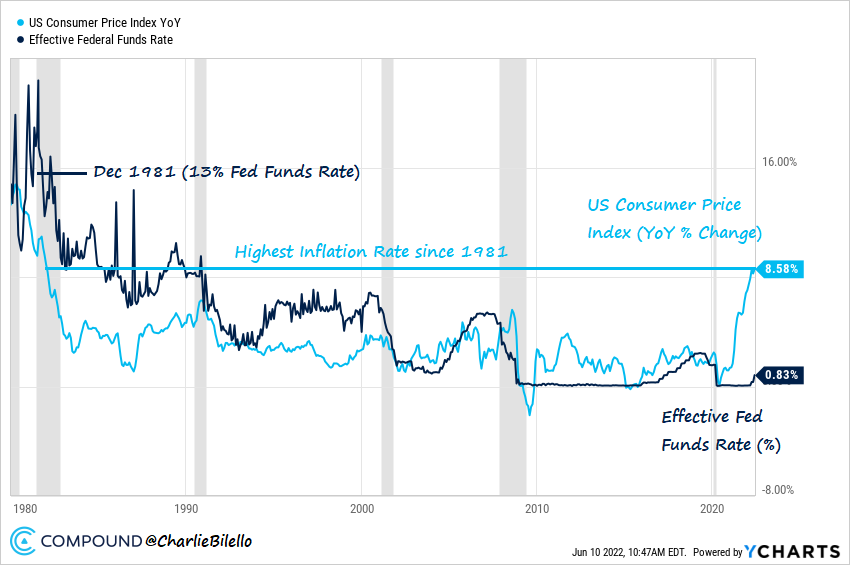

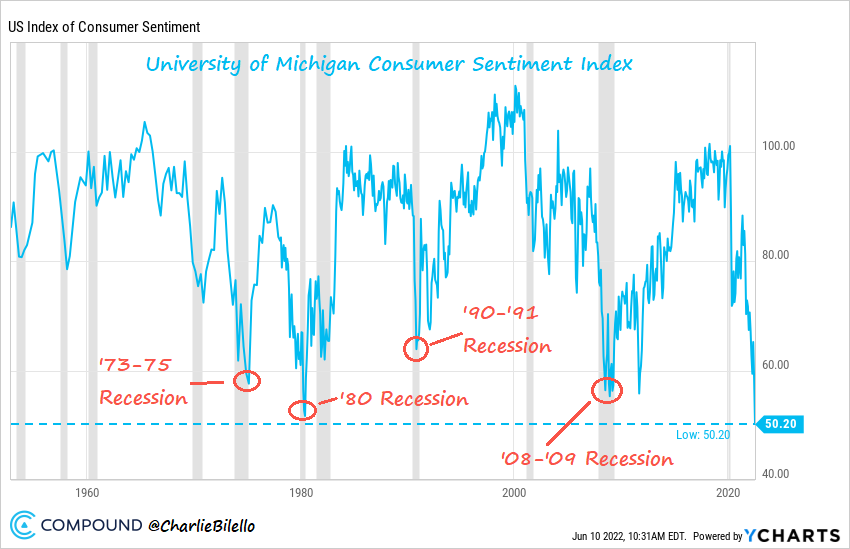

This is historically bad. What is causing this? In my eyes, there are two boogiemen in the room: inflation and consumer sentiment. And both are connected at the hip. As inflation continues to terrorize…consumer sentiment will continue to crater.

High inflation + low consumer sentiment = no bueno mi amigo.

Just look at these two charts below (source: Charlie Bilello / subscribe to him if you don’t already). Inflation has screamed higher and consumer sentiment has plummeted.

I don’t think this is what Jerome Powell envisioned for ‘transitory’ inflation. But This is news to no one. The Fed is going to continue raising rates until inflation is at least flattening. But I’m not sure that will cure it. Supply chains will need to come back online.

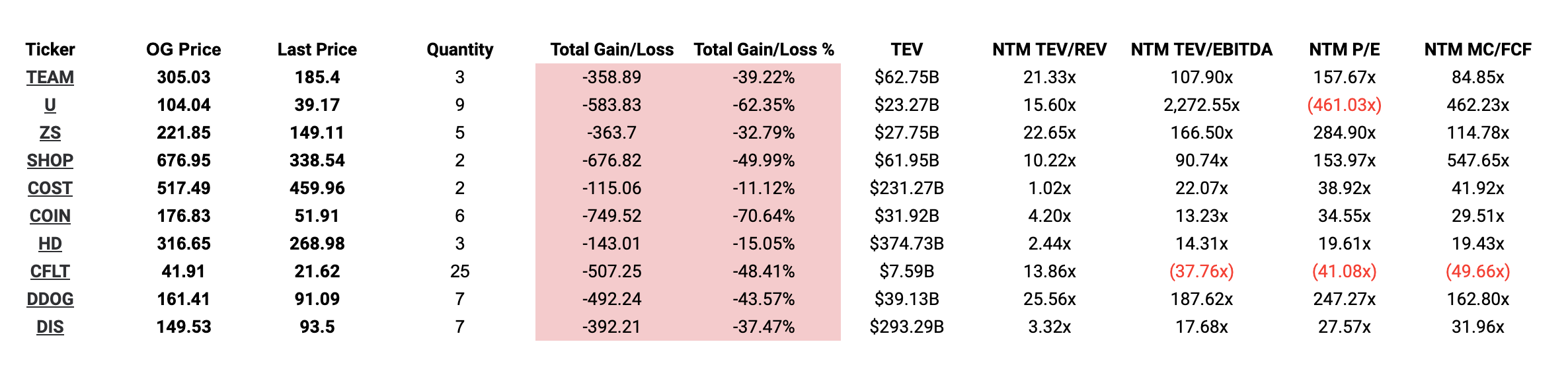

Enough with the macro. Let’s jump into the Q1’22 earnings for The Rookie Lineup companies. All of our companies have reported and here’s how they did:

The Rookie Lineup

TEAM - My thoughts on $TEAM’s quarter here: Earnings Extravaganza

U - Solid quarter. Really like this company. Stock price continues to fall, but the underlying business is strong and growing

Revenue was $320.1 million, an increase of 36% from the first quarter of 2021.

Create Solutions revenue was $116.4 million, an increase of 65%; Operate Solutions revenue was $184.0 million, an increase of 26%; Strategic Partnerships and Other revenue was $19.7 million, an increase of 11%, each as compared to the first quarter of 2021.

Loss from operations was $171.2 million, or 53% of revenue, compared to loss from operations of $110.9 million, or 47% of revenue, in the first quarter of 2021. These results were impacted by an increase in stock-based compensation expenses.

1,083 customers each generated more than $100,000 of revenue in the trailing 12 months as of March 31, 2022, compared to 837 as of March 31, 2021.

Dollar-based net expansion rate as of March 31, 2022 was 135% as compared to 140% as of March 31, 2021. NEED to watch this.

ZS - Leader in the SASE and Security space. This is a critical B2B software company for it’s customers and has pricing power

Revenue grows 63% year-over-year to $286.8 million

Calculated billings grows 54% year-over-year to $345.6 million

Deferred revenue grows 65% year-over-year to $818.7 million

Cash flow: Cash provided by operations was $77.2 million, or 27% of revenue, compared to $73.4 million, or 42% of revenue, in the third quarter of fiscal 2021. Free cash flow was $43.7 million, or 15% of revenue, compared to $55.8 million, or 32% of revenue, in the third quarter of fiscal 2021.

+125% Dollar-based Net Retention Rate

SHOP - Wonderful business that has been punished due to its valuation.

Revenue in the Q1’22 grew 22% to $1.2 billion, a two-year compound annual growth rate of 60%

Monthly Recurring Revenue was $105.2 million. MRR increased 17% year over year, up from $89.9 million

Subscription Solutions revenue was $344.8 million, up 8% year over year, primarily due to more merchants joining the platform

Gross Merchandise Volume was $43.2 billion, which represents a two-year compound annual growth rate of 57% and an increase of $5.9 billion, or 16% over the first quarter of 2021.

Gross Payments Volume grew to $22.0 billion, which accounted for 51% of GMV processed in the quarter

COST - Costco is not raising hotdog prices. Best company is America.

COIN - Rough. This one is rough. COIN is on thin ice. Their revenue is STILL TOO dependent on transaction fees. They need to use this Crypto-Winter to come back leaner, meaner and become THE platform of the future.

Here’s wonderful thread by Eugene Ng on Coin’s tough quarter

HD - You spend too many weekends here. Inflation will be tough for $HD as it impacts their supply chain and avg. consumer spend on DIY projects. But $HD will weather the storm and is a pillar of the economy.

Total sales growth and comparable sales growth of approximately 3.0 percent

Operating margin of approximately 15.4 percent

CFLT - These next 3/4 quarters will show how CRITICAL Confluent is within a customer’s tech stack. Is it business critical or a ‘nice' to have for developers? Things to watch are continued growth of $100k Customers and the NRR

Total revenue of $126 million, up 64% year over year

Confluent Cloud revenue of $39 million, up 180% year over year

Remaining performance obligations of $551 million, up 96% year over year

791 customers with $100,000 or greater in ARR, up 41% year over year

Dollar-based NRR for Confluent Cloud of greater than 150%. NEED to watch this.

DDOG - Chef’s kiss here. Touch macro environment, but this company is performing at a highlevel.

Revenue was $363.0 million, an increase of 83% year-over-year

2,250 customers with ARR of $100,000 or more, an increase of 60% from 1,406 YoY

GAAP operating income was $10.4 million; GAAP operating margin was 3%

Partnered with Microsoft for the Azure Cloud Adoption Framework.

DIS - The Mouse is having a tough time. They’ve got the strongest IP and brand in the game, and will get through this.

Get ready for Q2 earnings season. Warren Zevon is…