Spotify

Recently, this timeless song was shared with me:

I love this song. I hope you enjoy it as much as I do. Swing batter swing.

In other news, Onlyfans announced it would ban sexually explicit content beginning in October. Liberty Highlights had a good summary on this head scratching decision (you can read it here). And then…they changed their minds. Onlyfans is back.

The Premier League is underway and here are my takeaways. That stomach is amazing #poetryinmotion.

The Contenders

$MANU looks good but inconsistent. They need a defensive midfielder if they want to contend for the title. Man City needs some time to jell with Grealish, but they will be fine. Chelsea looked fantastic over the last 2 games and are going to be contenders in all of their tournaments.

Surprises

Tottenham has shown heart and resolve without Harry Kane and if they can sign Adama Traoré that would be a huge boost. Everton is playing a fun brand of soccer and I like their team.

West Ham looks solid, dangerous, and will cause problems for most teams this year.

Just Sad

Arsenal are trash.

This week we are going to be looking at Spotify ($SPOT). As a reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team. NOTHING HERE IS INVESTMENT ADVICE. DO YOUR OWN HOMEWORK.

Step 1: Do I understand the business?

I think everyone is familiar with Spotify and what it does. But here is how they describe themselves “Soundtrack Your Life. Spotify has transformed the way people access and enjoy music. Today, millions of people in 178 countries and territories have access to more than 70 million tracks, whenever and wherever they want. We are transforming the music industry by moving from a "transaction-based" experience of buying and owning audio content to an "access-based" model allowing users to stream on demand.”

And their mission statement “is to unlock the potential of human creativity by giving a million creative artists the opportunity to live off their art and billions of fans the opportunity to enjoy and be inspired by these creators”.

$SPOT is the largest subscription based audio streaming platform on Earth. They are available in over 93 countries, they have 365 Million MAUs, and have 165 Million Premium Subscribers. They have a huge subscriber based compared to their freemium user base.

This shows that $SPOT is successfully able to convert free users into paying users at scale. This is a fantastic flywheel for continued product adoption, usage, and revenue growth.

I really liked these two sentences on their go-to-market strategy, “The Premium Service and Ad-Supported Service live independently, but thrive together. Our Ad-Supported Service serves as a funnel, driving a significant portion of our total gross added Premium Subscribers”.

Enough with all of the business jargon…here is a great interview between Tim Ferris and Ek about $SPOT and dozens of other topics:

Verdict: Pass. I like their business and mission. I’m interested.

Step 2: Moat and Future Growth/Catalysts

Disclaimer: I’m not a user huge $SPOT. I use Amazon Prime music because it comes with my Prime Subscription or use my turntable for music. I never found the UX/UI experience of $SPOT great and in my opinion, it hasn’t gotten better.

With that said, let’s talk about the good stuff. $SPOT has a wonderful brand, huge user base, and has shown the ability to win. They are no longer focused solely on music and are now reaching into everything ‘audio’.

I like their two engine ability to generate revenue via Subscriptions and Advertising. It will be interesting to see how they grow the Advertising business as it only makes up ~10% of revenue.

They are expanding their ‘content catalog’ and making their content ‘exclusive’ a la Netflix or HBOMax. Everyone has heard about $SPOT’s exclusive deal with Rogan for $100M which doesn’t appear to be trending in the right direction.

Ideally these exclusive deals will bring premium ‘ears’ to the app. But growth via acquisition is DIFFICULT.

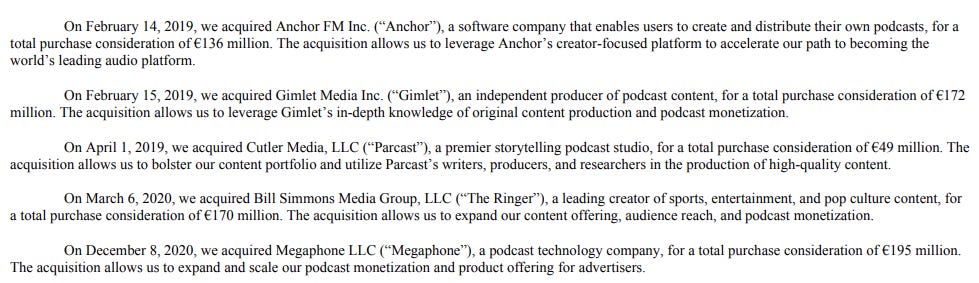

$SPOT needs to spend money to keep their flywheel spinning and keep premium users paying. Here is a list of some recent acquisitions from $SPOT

They are going after everything. And it shows in market share.

$SPOT estimates that the entire global music streaming revenue added up to $20B in 2019 and $SPOT made up $7.9B of that (~40% of the market revenue!).

$SPOT has tons of optionality to growth and expanding their MOAT.

If we look to their mission statement - “to unlock the potential of human creativity” -for guidance as to what they will do in the future, they could literally expand into anything related to audio (podcasts, live sports, radio, music, meditation, etc).

In short, $SPOT has a MOAT and it’s expanding, but can they maintain it and fight off competition?

Now, let’s get to the ‘tuff’ stuff:

Tons of Competition

Issues with the TAM size

Growth will be EXPENSIVE

User churn and slowed premium user conversion

$SPOT faces increasing competition as they expand further into everything audio. They are going head-to-head with the likes of Youtube, Tiktok, Apple, Google, Amazon, etc. to win ears. That is TOUGH COMPETITION.

Now let’s address TAM - $SPOT already makes up around 40% of the total music streaming revenue market - How much more can they take? Can we expect historical growth to continue in the future? The answer is NO and their numbers agree (Source: Tikr.com)

Revenue has slowed. Gross Margins are flat. What does this mean? This means that $SPOT needs to move into new markets and verticals fast.

How large is $SPOT’s Total Addressable Market? I’m not sure, but we need to believe in $SPOT’s ability to leverage it’s optionality in order to 1) increase their TAM and 2) execute in those new markets/verticals (i.e. LATAM and live sports).

Two other metrics I want to highlight about $SPOT

A decreasing in APRU (Average revenue per unit) which basically means they are earning less and less per user on their premium service. This isn’t necessarily bad as it could be explained by their expansion into emerging markets and aren’t able to charge the same for a customer in LATAM vs NAMER. But it is something to watch. (Source: Annual Report)

A huge dependence on their premium service for revenue. It currently makes up around ~90% of revenue (Source: Annual Report). Having concentrated revenue streams like this makes the business fragile to any changes or risks in the future.

The last negative I want to mention with $SPOT is how expensive their growth is going to be moving forward. $SPOT will have very limited organic growth moving forward.

We already know they will need to spend $$$$ for exclusive content. They will need to spend $$$ for maintaining brand awareness and fighting off competition. Does $SPOT really have the ability to outspend Google, Amazon, and Apple? I’m not sure I like those odds.

$SPOT will need to rely on it’s culture of innovation, creativity, and execution to beat the competition.

$SPOT is a bet on management and their ability to execute. This isn’t a bet on a better business model or anything like that — $SPOT is a bet on management.

Verdict: 0.5 points. $SPOT is a leader in the space, but will they be in 5-10 years.

Step 3: Management

Founder led and managed? Check. Daniel Ek is the founder and CEO. Martin Lorentzon is a co-founder and a director on the board.

Does leadership have skin in the game? Check. Ek owns around 8.07% and Lorentzon owns around 11.13%.

Do employees like working there? Check. $SPOT has a 4.2 rating on Glassdoor (from 742 reviews) and 94% of their employees approve of the CEO.

Quick note on Daniel Ek. He is a winner. Prior to founding Spotify in 2006, Ek founded Advertigo, an online advertising company acquired by Tradedoubler. He has had success at each of his stops.

I also particularly liked his story of how Spotify was founded:

Verdict: Pass. I like Ek and the people around him.

Step 4: Valuation

High-level Numbers

Market Cap: $41.45B

TEV: $40.1B

Gross PM: 26.4% (Not great)

Current Ratio: 1.26x

NTM Total Enterprise Value / Revenue: 3.23x

Quarterly Revenue Growth (yoy): 23.40%

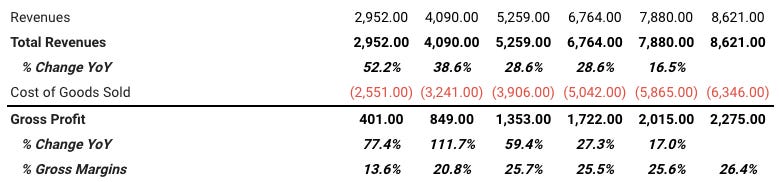

From 2016 to 2020, $SPOT grew their revenue from €2,952 to €7,880 (millions), and over the same period, their Gross Profit grew from €401 to €2,015 with a Gross Margins of around ~25%. This isn’t great for a SaaS based streaming platform. Netflix in comparison has a Gross Margin of around 35-40%.

They are free cash flow positive. They don’t have any debt.

I ran a ‘rough’ DCF with the following assumptions: a discount rate of 15%, growth rate of 30% (years 1-5) and 15% (years 6-10), and a terminal multiple of 5x. With these numbers, I got a rough range of $230 - $190. If you apply a 15% Margin of Safety you get a rough value of $165/share.

Currently, $SPOT trades at ~$226.90. This is 40% down from it’s all time highs back February of 2021. In just ~6 months, $SPOT has lost almost half of its market cap. Woof.

As with any valuation model, you could’ve applied other assumptions and ended up with different numbers. Everything is a ‘guesstimate’ when it comes to DCFs.

Verdict: 0.5 Pass. $SPOT is close to fair value. If $SPOT shows revenue growth moving out of COVID, this story gets a lot more interesting. NOT INVESTMENT ADVICE.

The Rookie Quick Fire Challenge - LINK HERE

Score 42 / 81

Overall Verdict: $SPOT is interesting. $SPOT is all about what story you apply to it’s valuation. It could become the biggest player in audio and consume the world and 5x from here, or it struggles to execute against increasing competition and has to spend everything it earns to maintain growth. I’m not sure, but at $40B, it feels undervalued. NOT ADVICE. THIS IS JUST FOR FUN.