The Rookie Checklist: MGM Resorts International

The Rookie Checklist: MGM Resorts International

$MGM, can the lion continue to roar?

The reopening trade is here. Inflation is getting spicy. Money is rotating from growth into value, and all of a sudden companies trading at +30x Price/Sales are out of favor - who knew valuations matter? The VIX is +$20, and CNN’s Fear and Greed Index seems to be flip-flopping every week.

So why choose MGM Resorts to study this week? I think the casino industry, specifically MGM, is a perfect metaphor for how we can understand what’s happening, and where things are potentially headed.

Reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team. I want to own my businesses forever.

As always, before we jump into the boring stuff, here’s what I’m jamming to:

Best album of all-time? Maybe.

Step 1: Do I understand the business?

MGM, as described by themselves in their latest 10Q, “owns and operates the following integrated casino, hotel and entertainment resorts in Las Vegas, Nevada: Bellagio, MGM Grand Las Vegas, The Mirage, Mandalay Bay, Luxor, New York-New York, Park MGM and Excalibur. Operations at MGM Grand Las Vegas include management of The Signature at MGM Grand Las Vegas” and several other MGM properties throughout the USA and international countries.

Their inspirational vision is “to be the world’s premier gaming entertainment company”, and they aim to achieve this based on 4 core strategic pillars: strong people and culture, customer-centric model, operational excellence, and disciplined capital allocation to maximize shareholder value.

I don’t love these strategic pillars. They are incredibly vague and boring - those could be copied and pasted from any other S&P 500 company, and you wouldn’t know the difference.

With that said, I like what I saw on the Key Q1 2021 Takeaways with growth from MGM China, expansion into iGaming, investment in digital transformation, and improved operational efficiencies.

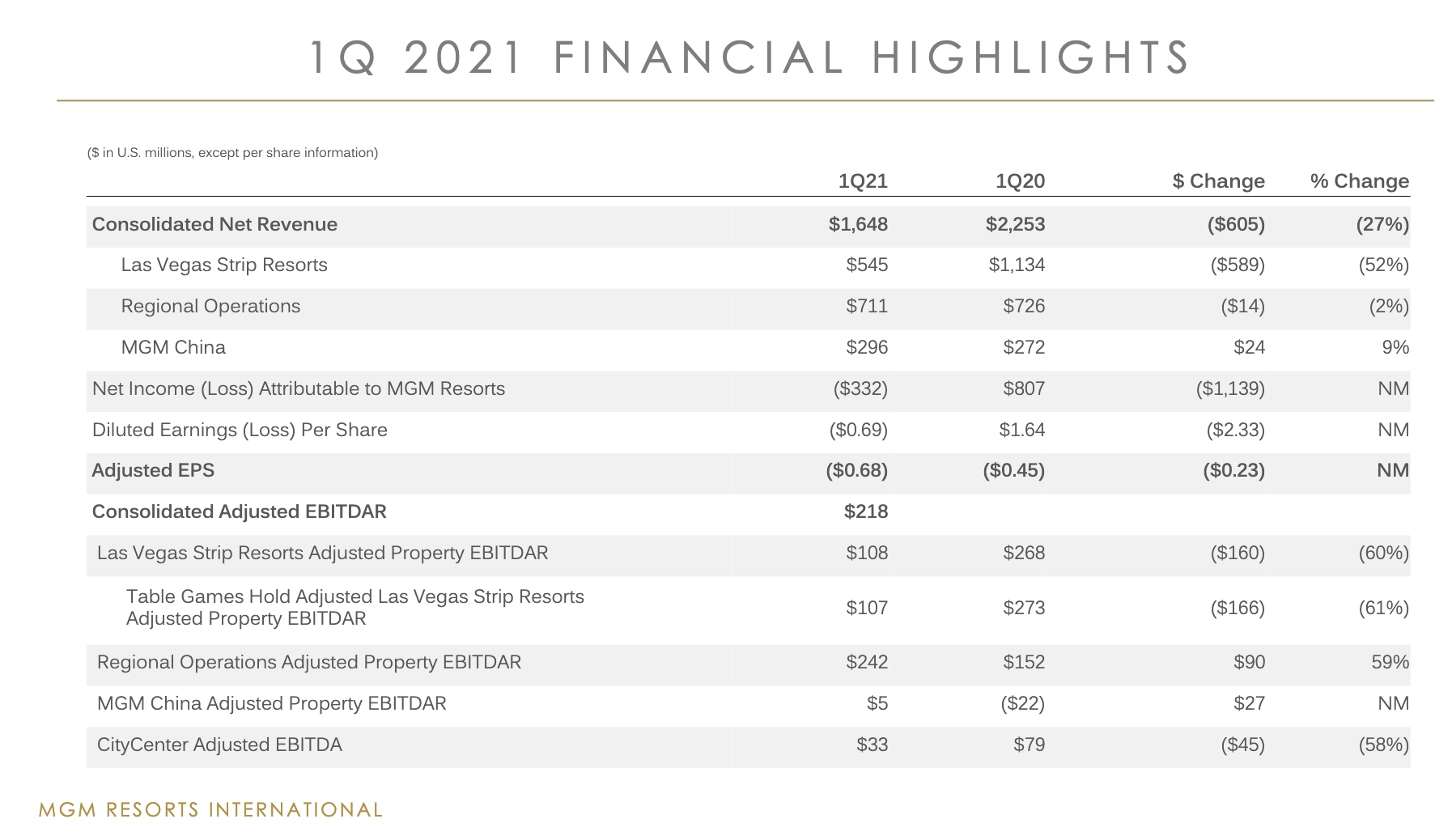

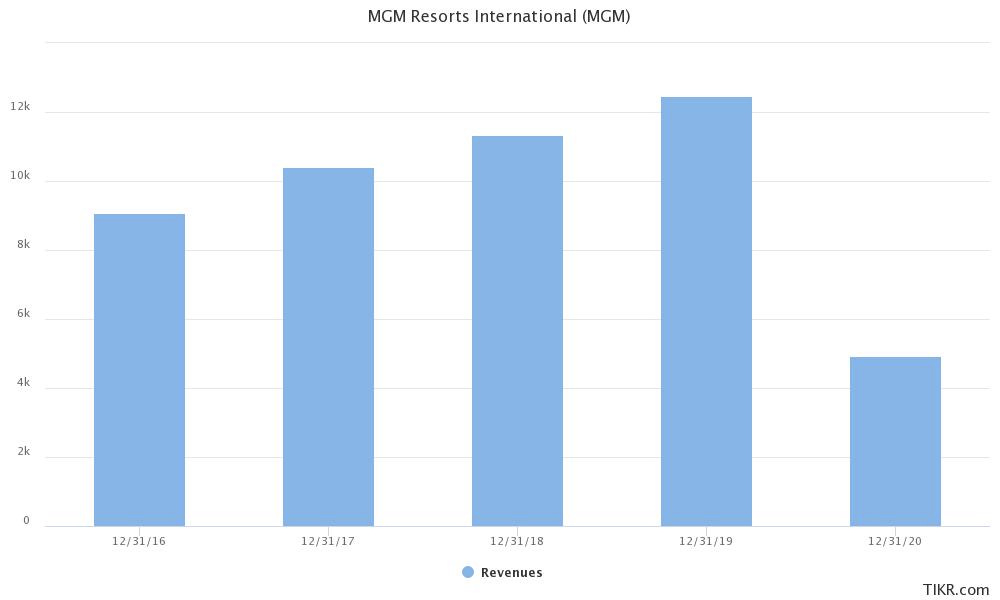

Here is a short breakdown of their recent revenue and where it comes from;

As everyone knows, MGM was absolutely slaughtered by COVID in 2020 and early 2021, but things are trending in the right direction with the re-opening and increase in vaccinations in the USA.

Even in the last few days, MGM [Nevada locations] have decided to open at full capacity without social distancing restrictions.

For me personally, this seems a bit early, and who knows if customers/travelers will be comfortable heading straight into a hotel without restrictions. I generally think the scars of COVID on society will be harder to shake / forget than businesses would like.

Go over to a friends house for an outside gathering - COUNT ME IN…Go to a packed hotel and casino with thousands of people I’ve never met - HARD PASS FOR NOW.

With that said, I think there is a large enough appetite that people are just waiting to travel. I think this is where my thesis lies and where my internal battle exists - even AARP is pumping Las Vegas for it’s community.

On one had, I think there is enough growth opportunity for MGM to warrant a higher valuation multiple, and on the other hand, I see a slower reopening than expected and I am hesitant that MGM can get back to 2019 revenue’s over the next 6-12 months.

Verdict: Yes, I like and understand the business.

Step 2: Moat and Future Growth/Catalysts

MGM has a moat and I believe the moat is expanding. Their moat consists of physical properties (i.e. Casinos), Brand and Customer Loyalty Programs, and BetMGM. They are gaining market share in iGaming, expanding their partnerships with professional sports teams, and earning increased market share in China’s gambling market (currently at 11.5%).

MGM’s latest IR presentation lays out future growth opportunities for the business: continued investment in MGM China and BetMGM (iGaming). MGM expects their BETMGM opportunity to generate +$1B in revenues by 2022, and are estimating a TAM of $32B for iGaming / sports betting.

MGM is well position to take advantage of the continued momentum of legalized sports betting / iGaming in the USA as they are currently leading in Michigan, Colorado, NJ:

The 2 questions I like to ask myself about Moats, are 1) is this company everywhere (or can it be?) and 2) Does this business have pricing power? Both of these questions help me centralized my thinking, and when using this framework to analyze MGM - I think MGM’s moat is large, expanding, but rather, thin and shallow.

Kind of like the shallow end of the pool, probably deep enough to keep small competition at bay, but definitely not deep enough to differentiate against larger competition or have the pricing power to gain a huge amount of market share.

You look at companies like Caesars Entertainment, Inc. ($CZR), Penn National Gaming, Inc. ($PENN), DraftKings ($DKNG), and you can see how more focused competition can start eating away at MGM’s moat.

Verdict: Pass…barely

Step 3: Management

First off, I love that $IAC is a 11.93% shareholder of $MGM (it may be smarter to own $IAC than $MGM directly - just an idea).

The CEO, Bill Hornbuckle, has been with MGM for over 20 years, has a +70% approval rating on Glassdoor, and is now battle hardened from COVID and steered the ship successfully through the last 12-18 months.

I think these two interviews do a good job of showing how this man operates at the worst of times and when the wind is at his back. He doesn’t give me the ‘hibbie jibbies’, and from what I have read online, he seems like a winner.

Verdict: Pass

Step 4: Valuation

High-level Metrics (as of May 17, 2021):

NTM EV / Revenue: 4.05x

NTM EV / EBITDA: 19.27x

Gross PM: 37.1%

ROC: (5.6%)

Current Ratio: 3.86x

I ran a couple scenarios, and this is what I am thinking:

Bull Case - MGM is firing on all cylinders (15% probability)

Casinos/hotels are fully open, events are happening, millions of tourists are walking MGM’s floors, and exceed 2022 revenue estimates of $11-13B by a significant margin

BETMGM continues it’s rollout out nation wide and takes dominate market share in North America as the home for all iGaming needs

MGM China continues its climb to 15% market share, and MGM looks to strategically expand internationally with additional casinos, and online gaming platforms

Bear Case - External pressures reign down and competition wins out (10% probability)

COVID variants spring up in both the USA and in China forcing MGM to slow down the reopening, scaring tourists from traveling, and continued limitations on capacity

BETMGM fails to take advantage of the iGaming market momentum and fumbles market share to competition that is more focused and has more technical expertise in technology / app building / network creation

China’s gambling market slows and flattens, and increased competition in the China market makes it impossible for MGM to win

Base Case (75% probability)

The reopening goes smoothly and traveling gets back to 2019 levels, and MGM is operating at expected levels (42.5% Gross PM, 13% EBIT Margins) and hitting revenue targets of $11-13B in revenue by 2022

BETMGM expands into new states as iGaming becomes legal, and takes #1 market share in the majority of the USA, and hits the +$1B in revenues by 2022.

MGM China continues its climb to 15% market share, and MGM looks to strategically expand internationally with additional casinos, and online gaming platforms

Based on these situations, I am ever-so-slightly bullish on MGM’s ability to execute on their strategic pillars. In the next 1-2 years, I think they fall somewhere in between the Base and Bull Case scenarios.

Based on comps like $CZR which trades at 13.81x NTM EV / EBITDA - this is cheaper than MGM - I think MGM is currently trading at it’s fair value. I don’t see a huge amount of down side, but I don’t see a large margin of safety either.

I think the upside is limited due to the high expectations of the ‘reopening’ trade being ‘baked-in’ right now, and if those expectations aren’t exceed over the next 1-2 quarters, there may be a slowdown in momentum.

Verdict: Meh - the next 2-3 quarters will provide a cleaner picture of the COVID situation and how MGM is executing on its strategic vision

The Rookie Quick Fire Challenge - LINK HERE

Score 37 / 81

Overall Verdict: I like the business, but it’s not hugely differentiated. Pass.