Zillow Group

Man, there are a lot of things happening.

Facebook went down and all of a sudden, people started to remember that life happens outside of their phones. Check out this piece by Cloudflare if you’re looking to understand what happened to Facebook.

NBA Preseason has started and Steph Curry looks ready. Poetry in motion.

The stock market is choppy and CNN Fear and Greed meter is at 25. Fear is in the markets: Will Evergrande have a butterfly effect and bring down world markets? Will the US treasury continue to rise? Will the US Gov’t crack down on tech? Will value start to outperform growth? Who knows…and who cares. Any one out there peddling they know or touting that you need to buy this company is full of crap. They are pests probably make most of their money from their follower base and substack subscription fees.

If you want a sanity check from the fintwit community, here is a video of Morgan Housel (he’s a complete stud) that is under 1 minute that applies to the majority of Americans:

I recommend checking out this longer podcast/video with Morgan and subscribing to his blog.

Do what works for you and YOUR goals.

For me - all I know is that by dollar cost averaging, focusing on high quality companies, and extending my ‘time in the market’ —> then history says I’ll make money and be wealthy in the long run.

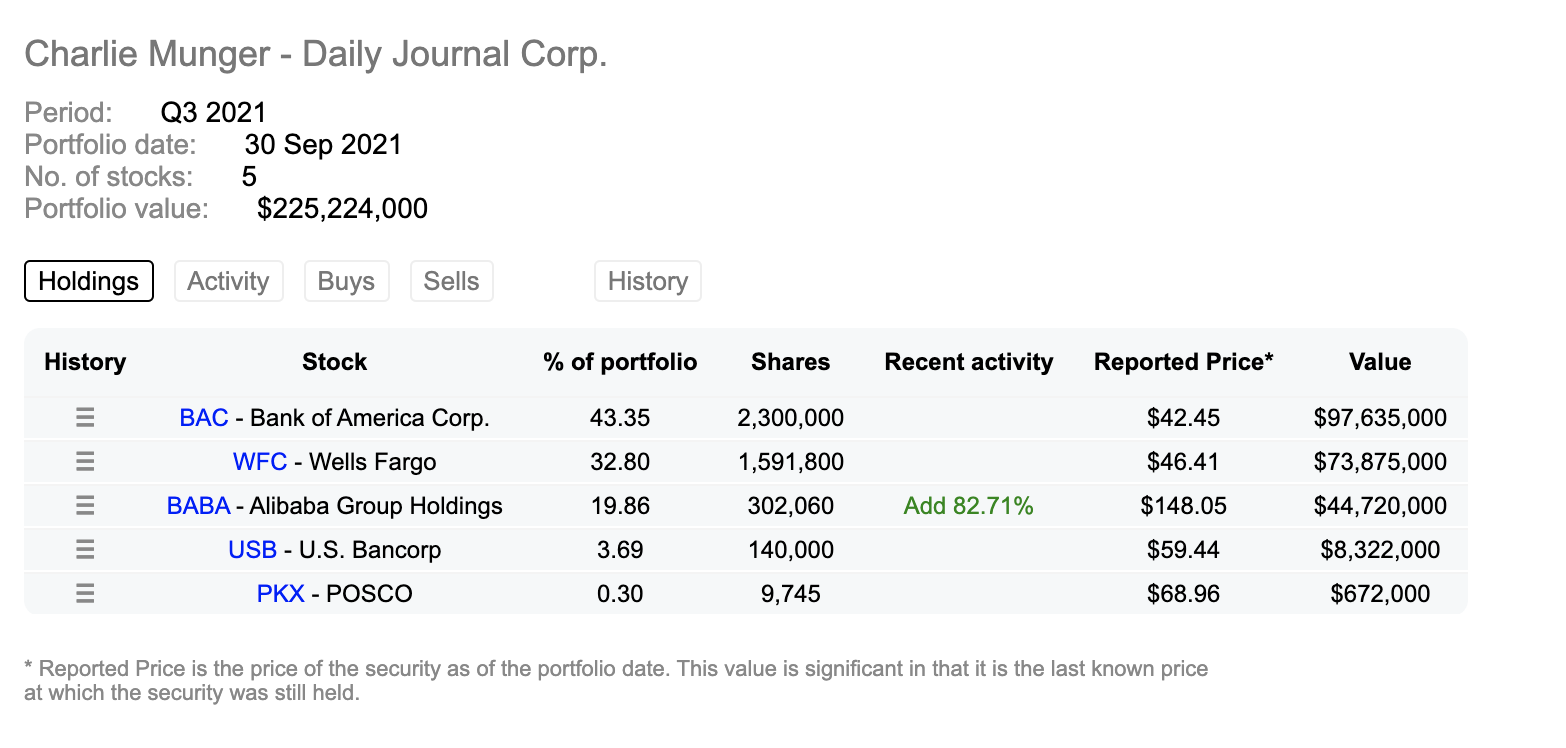

Here’s an example from one of the GOATs on ignoring the noise and following your own thesis - Munger just bought more $BABA. In the middle of the China storm, Munger buys more $BABA #tuff.

I thought this was an interesting chart in I/O Fund’s weekly piece by Knox Ridley: Sentiment Puts a Floor Under this Dip. The S&P 500 continues to climb, but the breadth of the increasing is not rising the tide for all boats. Is there market weakness under the surface? I don’t know - it’s probably more noise than signal, and too macro of information for me to do anything with.

On a personal note, life is good and I am grateful. I need to remember that more often.

This week we are going to be looking at Zillow Group ($ZG). As a reminder: The Rookie wants to own businesses that 1) I like, 2) are growing, 3) generate a high amount of free cash flow, 4) have future optionality, and 5) are led by a great management team. NOTHING HERE IS INVESTMENT ADVICE. DO YOUR OWN WORK.

Zillow Group ($ZG)

Step 1: Do I understand and like the business?

I’m bring an interesting perspective to the real estate game…I live in the Bay Area. And buying a home in the bay area is like trying to get laid in high school - it’s nearly impossible and you'll definitely no nothin’ about what you’re doing. And when it does finally happen, you probably don’t feel great about yourself.

Thanks for assuming me. Now back to $ZG.

Do I like and understand the business?

Everyone knows Zillow and their infamous Zestimate: it’s the favorite website of every 25-35 year old who likes to daydream about 3-car garages and fancy kitchens. Want to waste 20 minutes daydreaming about you dream home or snoop on your neighbor’s home? Go check out Zillow and click away.

But what does Zillow actually do? $ZG describes themselves “…as reimagining real estate to make it easier to unlock life’s next chapter. As the most visited real estate website in the United States, Zillow and its affiliates offer customers an

on-demand experience for selling, buying, renting or financing with transparency and nearly seamless end-to-end service”

Traffic to $ZG’s mobile apps and websites reached ~230 million average monthly unique users - damn, talk about reach. This is 5% growth YoY and up 10% from a year ago. Side not - it’s good to know I am not alone in browsing through $ZG’s inventory (biggest in the USA) in my free time.

But what does being “the most visited real estate website” actually mean? So what…and why do should we care?

The reason we care is because $ZG has gone through a major business transformation over the last 2 years. $ZG’s management team made a big bet to evolve from a search-and-find real estate marketplace (i.e. most revenues coming from ads, etc) to participate in the real estate transaction itself (i.e. most revenues coming from ‘Homes’ and ‘IMT’).

$ZG breaks their revenue in three segments: the Homes segment, the Internet, Media & Technology (“IMT”) segment and the Mortgages segment (Source: $ZG, 10Q, Q2 2021).

Homes = financial results from Zillow Group’s purchase and sale of homes directly through the Zillow Offers

IMT = financial results for the Premier Agent, rentals and new construction marketplaces, as well as dotloop, display and other advertising and business software solutions

Mortgages = financial results for mortgage originations through Zillow Home Loans and advertising sold to mortgage lenders and other mortgage

professionals.

Q2-2021 was a huge quarter for $ZG.

And I highly recommend reading through their Q2-2021 Shareholder letter to learn more about their revenue segmentation and business overview.

In short, Rich Barton, Co-Founder & CEO, and Allen Parker, CFO summed it up well “We’ve made big bets on the e-commerce future of the real estate industry. And every day we edge closer to realizing our dream of delivering a seamless, integrated, perhaps even joyful experience for our customers and partners.”

And this seems to be true. There are now countless stories of consumers going through $ZG’s entire distributed platform - from searching for a home, to getting the loan , and to finally purchasing the home - all through $ZG.

Welcome to the future.

Verdict: Solid- Pass. I like the business and I can understand it.

Step 2: Moat and Future Growth/Catalyst

Let’s start with the good.

Future Growth/Catalyst

$ZG is riding a wave - a housing wave.

If you haven’t been following the news, the USA is in a housing crisis. US Housing Market is in a secular bull market.

Builders can’t build fast enough, buyers are getting forced to pay higher and higher prices due to the nationwide housing market, and $ZG is primed to take advantage. \

And this is going to last years, “The total number of homes for sale rose 3.3%. Much of that inventory gain, however, came from new homes that have not yet been started or homes that are still under construction. Prices are still rising rapidly. On a year-over-year basis, the median new-home price rose 20.1% to $390,900” (www.kiplinger.com).

According to $ZG, their TAM (total addressable market) is enourmous. They are targeting several destinct markets

The $2.2 trillion in annual home sales (according to the 2020 US Census Bureau and National Association of Realtors®. And it’s not only selling homes

The $156 Billion U.S. Mortgage industry

The $32 Billion U.S. rentals marketplace, and everything ancillary to home insurance, home warranties, etc.

Growth - check.

But what does $ZG’s moat look like.

$ZG is a leader in their space. They have a NPS = 35 which is better than it’s main competitor, Redfin (NPS = 21). Accordingly to the 2020 Google Trends report, ‘Zillow’ is even searched more frequently than ‘real estate’. Read that sentence again. I LOVE this.

Taking over mindshare and mental space in consumers is a MOAT. Once habits develop, they are hard to shift and even harder for competition to chip away at.

$ZG’s business platform is also defensible. They have the largest housing database in the USA. Having the largest and broadest marketplace is a MOAT and it keeps consumers locked in.

MOAT - check.

Risks

One big RISK is being so correlated to interest rates and the housing market. No matter how strong it looks - do I really want to be so closely connected with the US housing market?

Another risk - competition. $ZG may be the leader in online real estate, but they face competition in every direction. They face competition from traditional players. And they face competition from similar online based companies.

Redfin, $ZG, and the traditional realtor ecosystem, will battle it out for marketshare. Eventually each one carves out their own niche of the market and we’ll end up in a tri-opoly. We see this in almost every industry: Airlines, Consumer Goods, etc.

I actually don’t think competition is $ZG’s biggest risk.

$ZG biggest risk is brand erosion and government intervention. As I’ve been doing more and more research on $ZG, there is a common hate, distrust, and fear from the general population of $ZG’s business practices.

It is becoming evident that $ZG’s business practices of buying up properties is NOT good for the every day consumer.

People are getting priced out of neighborhoods, because $ZG controls the market and the pricing. The very consumer that wants to buy homes on $ZG is getting priced out by $ZG.

Who knows if the government will step in on this? Probably not, but it’s something to consider on a state by region basis.

$ZG’s brand erosion won’t happen over night, but buyers are getting tired of paying more $$ for less.

Verdict: Solid - Pass

Step 3: Management:

$ZG’s employee’s love working there. And 95% of $ZG’s employees ‘approve of the CEO’ (based on 263 reviews). That is HUGE.

Rich Barton is co-founder and CEO, and Lloyd Frink, is co-founder and Executive Chairman. If you read my shit regularly, I love co-founders still being involved in the company.

Do they have skin in the game? Barely. Barton owns 0.62% of $ZG and Frink owns 1.07%. It’s better than nothing, but not a huge amount all considered.

Another thing to note is that Greg Maffei owns 0.51% of $ZG. It’s generally been a good decision to align your money with Maffei.

Everything on Barton seemed fantastic and I love this quote to shareholders:

“And while cyclicality in the housing market affects us, we believe our vision to come down the funnel and streamline the real estate transaction for customers and agents will drive our secular growth in the future. As we continue to innovate around the customer transaction experience, we expect to grow the small share of transactions we are currently involved with by continuing to broaden our services and increasing the number of services each of our customers use per transaction.”

I like the talent Barton and Frink have surrounded themselves with. David Beitel, CTO, was formerly the CTO of Expedia before $ZG, and Allen Parker, CFO, was vice president of finance for Amazon Devices, Appstore & Amazon Pay prior to joining $ZG.

Winners win.

Verdict: Fantastic

Step 4: Valuation

High-level Numbers

$23B Market Cap

$21.2B Enterprise Value

50.7% LTM Gross Profit Margins

3.82x Current Ratio

2.49x NTM Enterprise Value / Revenue

The main reason I got interest in $ZG is because it’s down 55.1% from it’s ATHs in February 2021. Has the business really gotten 50% worse?

I don’t know, but when I look at $ZG is looks cheap considering it’s growth potential. Let’s look at the valuations of $ZG and $RDFN to see if that helps:

From a valuation point of view, they are comparable, but to be honest, I like $RDFN coming from a smaller market cap. This didn’t help.

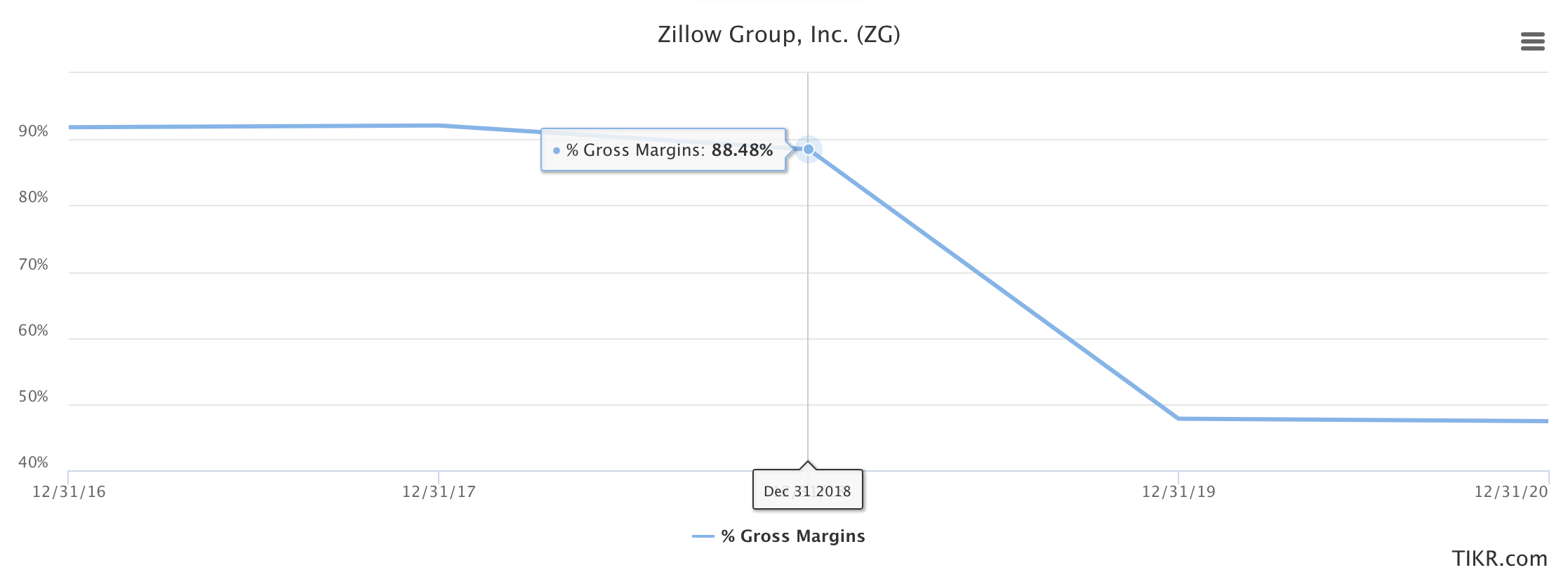

With the said, let’s run the numbers. From 2016 to 2020, $ZG grew revenues from $846M to $3.4B all while operating at around ~50% Gross Profit Margins.

The interesting thing is you can see where $ZG shifted it’s business model from being a pure-play advertising marketplace to becoming an end-end real estate engine:

In 2018, $ZG shifted to becoming the end-to-end solution and it ate away at the Gross Profit Margin, but it expanded $ZG addressable market and supercharged their revenue+earning potential.

Pay now, and get paid even more down the road.

As always, I like simple math. I ran a ‘rough’ DCF with the following assumptions: a discount rate of 10%, growth rate of 40% (years 1-5) and 20% (years 6-10), and a terminal multiple of 5x. With these numbers, I got a rough range of $163- $141. If you apply a 15% Margin of Safety (on the low end) you get a rough value of ~$120/share.

Currently, $ZG trades at ~$91.

As with any valuation model, you could’ve applied other assumptions and ended up with different numbers. Everything is a ‘guesstimate’ when it comes to DCFs.

Verdict: Pass. $ZG isn’t cheap by traditional metrics. But it’s reasonable considering it’s future growth potential.

The Rookie Quick Fire Challenge - LINK HERE

Score 48 / 81

Overall Verdict: I like $ZG a lot. They are a leader in a growing market and well positioned to take advantage of any tail winds. With that said, $ZG is very correlated to market sentiment and increasing interest rates, and other macro tends (i.e. government regulation). $ZG isn’t constantly free cash flow positive and this needs to change. BUT at this valuation, $ZG offers a solid risk-reward. THIS ISN’T INVESTING ADVICE. GO DO YOUR OWN WORK.

Other things that need investigating:

Understanding $ZG’s competitive edge compared to $RDFN. Who wins the future?

What does $ZG look like in 5 years?

What happens if interest rates increase?

Do I want to be aligned with the US Housing Market? 2007-2008 is knocking at the door…

If you want to learn more about $ZG, check out this interview between Chit Chat Money and Brian Feroldi: