The Rookie Challenge

The world is a mess - let’s start with jams first:

Fucking so groovy

This post is the start of a change.

Instead of writing about a random company for each post (a recent one was done on Coinbase) and giving it a Rookie Score (The Rookie Checklist Part 1 and The Rookie Checklist Part 2), I am going to select 10-15 companies to focus on for the remainder of the year.

I am planning to follow these 10-15 companies throughout the year and track their performance against the SPY ETF.

Can these 10-15 companies beat the S&P 500? Who knows, but it should be fun.

Where did I get this idea from?

I’m a fan of Warren Buffett. I read his annual letters and I’ve read countless books about him and his investment style. Specifically, I’ve always gravitated to his idea of an ‘investing punch card’. The basic premise is that YOU as an investor get to select 20 investments over a lifetime and only those investments.

Why do this?

This exercise forces me to focus. AND be strict with my ideas. It forces me to (hopefully) choose the best companies.

What can you expect?

Over the next 10 months, I will be tracking everything these 10-15 companies do: from Quarterly Reports to Press Releases , I will be tracking it here and updating my thesis on each company.

Why these companies?

I wanted to build a portfolio that offered me a good combination of diversification, growth, and safety. And this is why you see everything from Shopify to Home Depot.

If I had chosen 11 of my FAVORITE companies, you’d see way more Cloud Computing and SaaS companies, but that would concentrate me too much towards high-valuation businesses. OR I could have only chosen Dividend Aristocrats and more established companies, but this may have limited my upside.

Portfolio Construction: I will use the price as of 2/28/2021 for each of the individual companies below and equally weight each company.

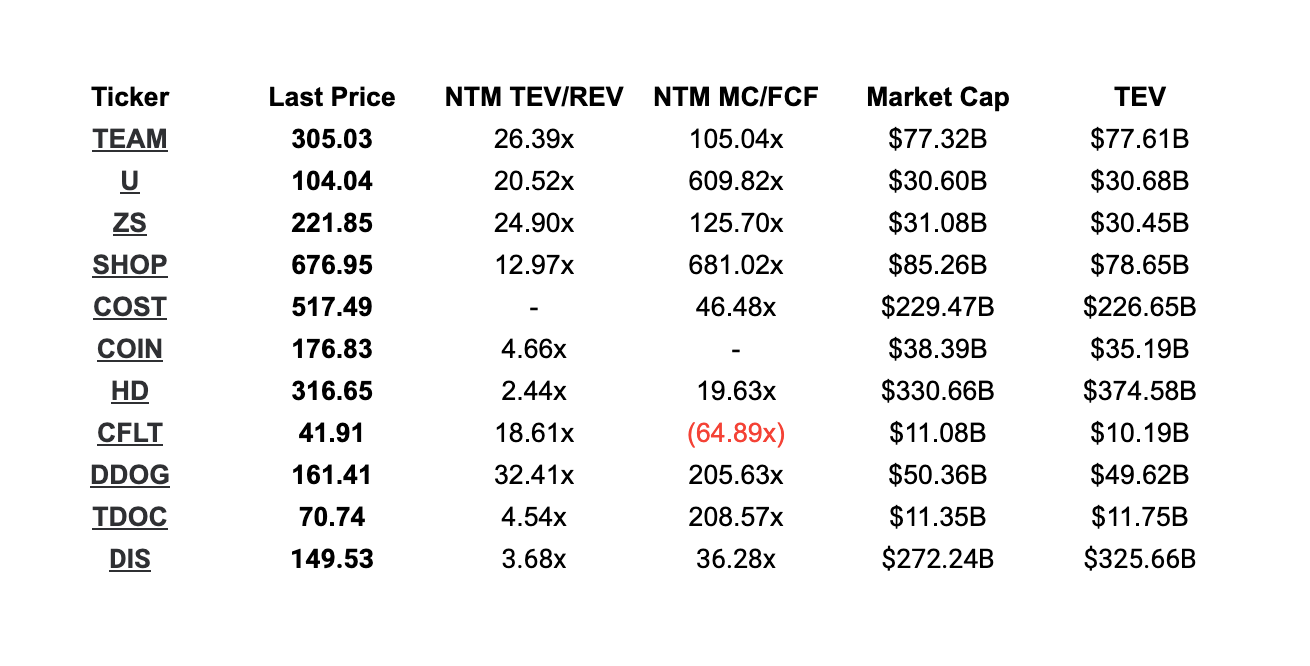

I see companies like $TEAM, $U, $ZS $CFLT, $DDOG as my high-flyers, but they have the potential for large losses. And I’ve planned to balance this out with the likes of $COST, $HD, and $DIS who will help with downside risk, and also offer solid growth prospects.

The Rookie Punch Card

The Starting Line Up (11):

Atlassian (TEAM)

Unity (U)

Zscaler (ZS)

Shopify (SHOP)

Costco (COST)

Coinbase (COIN)

Home Depot (HD)

Confluent (CFLT)

Datadog (DDOG)

Teladoc (TDOC)

Disney (DIS)

Atlassian (TEAM)

Why: Atlassian is a B2B Software company that provides workflow management systems, and other software solutions for over 200,000 customers worldwide. $TEAM is extremely sticky, has fantastic gross margins, is Free Cash Flow positive, is growing it’s top line at 30% YoY, and it’s run by an amazing management team

Risks:

Growth slows down

Competition eats away at margins

Trades at an expensive multiple: ~32x Price / Sales

Unity (U)

Why: Unity is a video game software developer, and it best known for it’s license game engine used to create video games, and other products. Unity is growing at ~43% revenue QoQ, has a Dollar-based Net Expansion Rate of 140%, and the Unity Engine is the most popular third-party game development software amongst developers worldwide.

Risks:

They are not profitable and probably won’t be for a while

Revenue Concentration: They make around 64% from their Operate Solutions1

Trades at an expensive multiple: ~28x Price / Sales

Zscaler (ZS)

Why: Zscaler is a cloud security company that specializes in Zero Trust. They are a leader in the Zero Trust security space, have over 250 customers with >$1M ARR, +1700 customers paying over $100k ARR, and a >125% Dollar-Based Net Retention Rate

Risks:

Trades at an expensive multiple: ~35x Price / Sales

Tons of competition in the Zero Trust and Cloud-Security Space

Shopify (SHOP)

Why: Shopify is an e-commerce platform that helps online retailers setup and create online stores for payment, marketing, shipping, and customer engagement tools. Shopify is growing rapidly with a total revenue of $4.7B for 2021 which was a 57% increase over 2020, has an extremely sticky and growing merchant user base, and is becoming an inevitable platform for buyers and sellers.

Risks:

Trades at an expensive multiple: ~19x Price / Sales

Increased competition from Amazon, Etsy, Wix, Squarespace, etc.

Confluent (CFLT)

Why: Confluent is a B2B software and data platform that offers real-time data integration, and analytics for organizations. Confluent is growing incredibly fast with 200% YoY revenue growth, has +700 customers with >$100K ARR, and a Dollar-Based Net Retention rate of 130%.

Risks

Trades at an expensive multiple: 21x Price / Sales

Potential large customer concentration risk (fading away, but need to see more >$1M ARR customers)

Large losses from operations and Free Cash Flow negative

Competition - Azure, AWS, GCP, IBM

Costco (COST)

Why: Do I really need to answer this? When did you last visit a Costco and spend less than $100 - nuff said. I love Costco and everything about them. And here is a podcast on why they are so amazing.

Risks

Slowed consumer spending due to inflation

Law of Large Numbers: How much can Costco continue to grow in the USA? Will they be able to replicate their success internationally?

Coinbase (COIN)

Why: See my write up HERE and did you see their recent Super Bowl ad - fire.

Home Depot (HD)

Why: Similar reason to Costco. They are dominate in their industry and the housing and DIY industries in the USA have clear tail-winds.

Risks

Slowed consumer spending due to inflation

Law of Large Numbers: Did COVID pull-forward all of their growth? If people aren’t locked up at home 24/7, will they continue spending so much on their homes?

Datadog (DDOG)

Why: Datadog is a B2B Software platform that offers observability service for cloud-scale applications, providing monitoring of servers, databases, tools, and services. Datadog is operating on all cycliners. In Q4’21, they grew revenue at 84% to $326 million, have +200 customers paying >$1M ARR, and a Dollar-Based Net Retention rate was above 130%.

Risks

Trades at an expensive multiple: 49x Price / Sales

They have large operating losses, but are Free Cash Flow positive

Teladoc (TDOC)

Why: Teladoc is a telemedicine and virtual healthcare company that helps connect patients, and healthcare providers. Teladoc is the WORST company on my list, but after dropping 75% from All-Time Highs, I think Teladoc offers a good risk-reward option here. Teladoc grew revenues in Q4’21 by 41% to $554.2 million, and continued to see success in Paid Members, Average US revenue per member, and number of visits.

Risks

Limited technological MOAT

Increased competition from companies such as UnitedHealth Group, Amazon, CVS Health

Slower than expected growth in paid membership

Operating losses continue and profitability may be several quarters away

Disney (DIS)

Why: Disney is everywhere.

Risks

Disney+ slows on subscription growth and/or consumers’ start to churn off the platform

Inflation slows down consumer spend

Law of Large Numbers: Can Disney continue to create magic at this size and scale?

SaaS Business Metrics I Care About

Revenue Growth QoQ

Dollar-Based Net Retention

Gross Margins

Large Customer Growth (>$100k ARR, >$1M ARR)

Customer Acquisition Cost (CAC)

Rule of 402 (if Applicable)

On the Bench:

Watchlist: Hubspot, MongoDB, Snowflake, Salesforce, Nike, Target

iShares Biotechnology ETF (IBB)

AdvisorShares Pure US Cannabis ETF (MSOS)

iShares U.S. Home Construction ETF (ITB)

WisdomTree Cloud Computing Fund (WCLD)

iShares Expanded Tech-Software Sector ETF (IGV)

What’s Next

In March, I will provide an update on each of these companies, and I will start tracking performance. See you then.

Disclosure: This is NOT investment and/or financial advice and shouldn’t be used as such. This is for entertainment purposes only.

Disclosure: I am long COIN, TDOC, DDOS, SHOP.

The Unity platform consists of two distinct, but connected and synergistic, sets of solutions. Our Create Solutions are used by content creators—developers, artists, designers, engineers, and architects—to create high-definition, real-time 2D and 3D content. Our Operate Solutions offer customers theability to grow and engage their end-user base, as well as run and monetize their content with the goal of optimizing end-user acquisition and operationalcosts while increasing the lifetime value of their end-users

Rule of 40 shows LTM growth rate + LTM FCF Margin. FCF calculated as Cash Flow from Operations - Capital Expenditures…here is so more background on the Rule of 40