The Rookie Challenge (March 1 - 17)

The Rookie Challenge (March 1 - 17)

What's happened - News Updates

Jams first:

Got 3 hours to kill? Tim Ferriss and Morgan Housel had a deep conversation about life, money, and everything in-between. I’m still digesting it, but it was well worth the time.

I’ve been on a Morgan Housel binge, and just finished his most recent book The Psychology of Money: Timeless lessons on wealth, greed, and happiness, and highly recommend it. In true Housel fashion, the book is clear, to-the-point, and concise on how to think about money and happiness.

Starting Lineup Performance and Valuation

Ouch, that is a lot of red. #investingishard

When will the pain stop? Is this a BTFD situation or are we entering a long tortuous bear market? Or do I dare say it, are we entering a recession…? The dreaded ‘R’ word.

Recessions are awful for all kinds of reasons - job loss, quality of life deterioration, etc. But from an investment perspective, the problem with recession is that we never know they’ll end. Recessions aren’t straight declines, and instead, during a recession there are tons of ‘head fakes’ or the disastrous ‘bear market rally’.

Just look at the chart below: there are going to be major swings to both the UPSIDE and DOWNSIDE during bear markets and recoveries1.

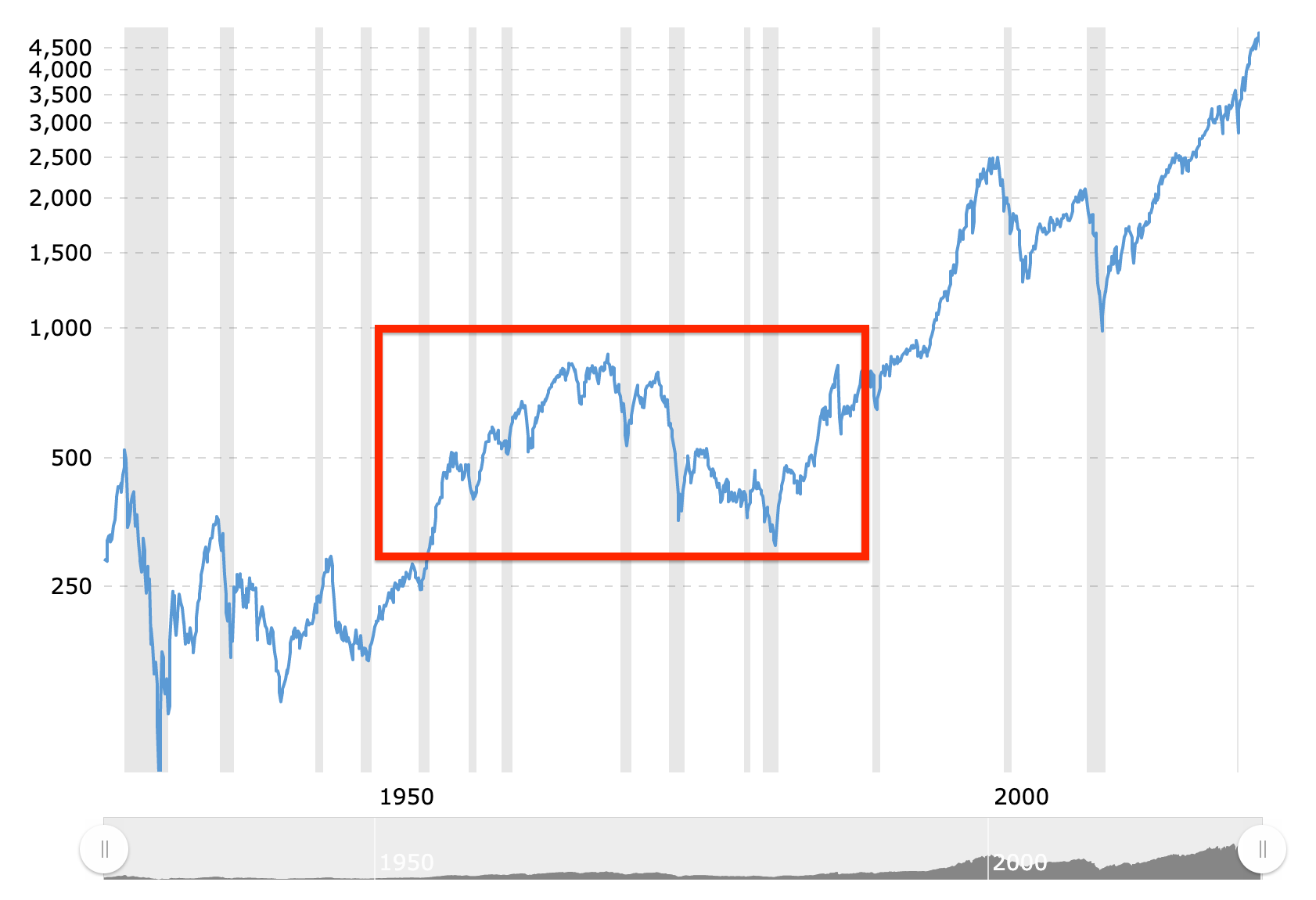

Here’s another one. Just look at this murderous chart below: This is the S&P 500 Index - 90 Year Historical Chart. If you zoom out far enough, the market will reward you over time. BUT if you focus on the red box from ~1950 —> ~1987 the market basically went NOWHERE.

That’s +30 years of basically NO returns. No me gusta.

Who knows what the market will do over the next decade, but I think there’s 3 main lessons here:

Timing the market is pointless

BTFD is not an investment strategy

The market will reward those who let TIME compound for them

SOO what are we supposed to do?

Well, Nick Maggiulli helps put things in perspective and his recent post, “Great Depression or Bust” couldn’t have been more timely - here is a fantastic blurb on what historical data tells us about times like these:

If a market decline does not lead to the next Great Depression (or similar event), then you probably got all worked up for nothing. And if it does lead to the next Great Depression, then your portfolio will probably be the least of your worries. Why? Because your financial assets will probably matter far less to you than your job, your ability to get food, and much more.

In other words, it’s Great Depression or bust. And even if we experience a crash like the Great Depression once again, how much will your portfolio actually matter? It probably won’t. It’s similar to the idea of investing during the Apocalypse. Unless your asset allocation contains canned goods, guns, or private farmland, it’s irrelevant.

Thankfully, when it comes to “Great Depression or bust”, most of the time the answer is bust. Most of the time a market decline does not become a once-in-a-century kind of event. No, most market declines are far tamer. This doesn’t imply that these tamer declines can’t have devastating impacts on the economy, they definitely can. However, as the data suggests, their impact on market prices tends to be short-lived.

Reminder - None, and I mean NONE of this is investment and/or financial advice.

The Starting Lineup:

Atlassian (TEAM)

Unity (U)

Zscaler (ZS)

Shopify (SHOP)

Costco (COST)

Coinbase (COIN)

Home Depot (HD)

Confluent (CFLT)

Datadog (DDOG)

Teladoc (TDOC)

Disney (DIS)

Earnings season is basically over. Here is a quick rundown of how our Starting Line-Up reported:

Atlassian (TEAM)

Rev $614m +33%

Gross Profit $516m +34% on 84% margin

Adj EBIT $166m +58% on 27.1% margin

Net Income $118m+54% on 19% margin

OCF $78m -1% on 13% margin

FCF $59m -2% on 10% margin

Thesis Killer: Nope, $TEAM is a beast. Not perfect though. I’d like to see a positive trend in FCF and revenue needs to continue at +30% (ideally high 30s).

Unity (U)

Rev $315.9m +43%

Dollar-Based Net Expansion was 140%

Thesis Killer: Nope. $U is expanding it’s moat. Need to watch operating expenses and ability to become profitable (or at least a vision towards that). And continued adoption of different revenue streams.

Zscaler (ZS)

Revenue grows 63% year-over-year to $255.6 million

Calculated billings grows 59% year-over-year to $367.7 million

Deferred revenue grows 70% year-over-year to $759.9 million

GAAP net loss of $100.4 million compared to GAAP net loss of $67.5 million on

a year-over-year basis

Non-GAAP net income of $19.2 million compared to non-GAAP net income of $14.0 million on a year-over-year basis 2

These Killer: Nope. $ZS faces tons of competition, but the TAM is huge. Things to watch are COGS increase, and competitions’ product development.

Shopify (SHOP)

Revenue was $1,380.0 million, a 41% increase

Subscription Solutions revenue was $351.2 million, up 26% year over year,

Merchant Solutions revenue was $1,028.8 million, up 47% year over year

MRR was $102.0 million, surpassing $100 million for the first time. MRR increased 23% year over year

Gross profit grew 37% to $692.7 million in the fourth quarter of 2021

Thesis Killer: Nope, but I see a lot of pain with $SHOP. $SHOP may be one of business in the world, but high multiples are out of favor with the market right now.

Costco (COST)

Revenue 51.9B up15.94%

Net income 1.3B up 36.59%

Net profit margin 2.5% up 17.92%

Operating income 1.81B up 35.22%

Cost of revenue 45.52B up 16.48%

Thesis Killer. Nope. Love me some $COST. This is a business that can thrive in any economy. Things to watch are COGS and how inflation impacts consumer spending (even though $COST is well positioned for a high-inflation envirnonment).

Coinbase (COIN)

Rev $2.5b +327%

Adj EBITDA $1.2b +319% on margin 48%

EBIT $922m +307% on margin 37%

Net Income $840m +375% on margin 34%

Thesis Killer: Nope. $COIN is a leader, they are growing, and they finically stable. Things to monitor are continued adoption of cryptocurrency and $COIN ability to expand it’s revenue PAST transaction fees. (Here’s a shallow deep dive I wrote on $COIN)

Home Depot (HD)

Revenue 35.72B up 10.72%

Net income 3.35B up 17.33%

Net profit margin 9.38% up 5.87%

Operating income 4.82B up 6.09%

Cost of revenue 23.86B up 11.33%

Thesis Killer: Nope. $HD is a staple in American and synonymous with our culture. Things to watch are COGS and consumer spending for DIY / home-improvement projects as inflation continues to wreck havoc.

Confluent (CFLT)

Revenue $120 million, up 71% year over year; fiscal year 2021 revenue of $388 million, up 64% year over year

734 customers with $100,000 or greater in ARR, up 43% year over year

Thesis Killer: Nope. $CFLT is growing and continuing to grow. Things to watch are 1) Sales and Marketing costs for that explosive growth, 2) DBNR numbers, 3) continued product development.

Datadog (DDOG)

Revenue grew 84% year-over-year to $326 million

Growth in larger customers, with 216 $1 million+ ARR customers, up from 101 a year ago

Achieved FedRAMP moderate-impact authorization

Launched Sensitive Data Scanner

Thesis Killer: Nope. Datadog is a good dog.

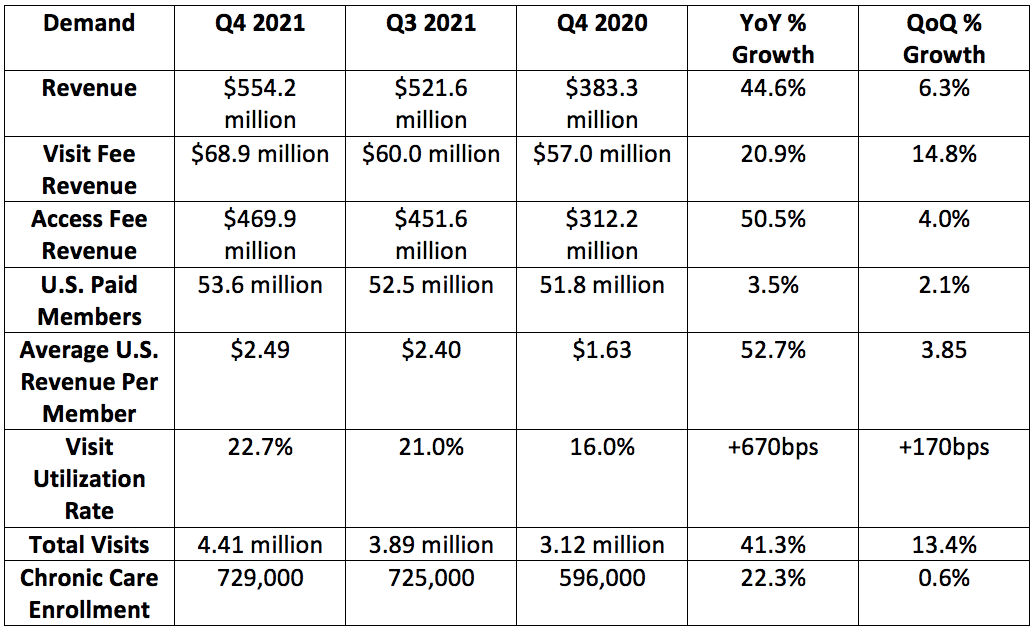

Teladoc (TDOC)

Thesis Killer: Not yet. $TDOC need to prove that it can continue to grow revenue, expand it’s moat, and that telemedicine really is the future. It was great to see that Teladoc partners with Amazon on smart speaker medical calls - this shows that Amazon didn’t want to do it themselves and that maybe $TDOC does have a technological moat.

Disney (DIS)

Revenue 21.82B up 34.28%

Net income 1.1B up 6394.12%

Net profit margin 5.06% up 4960%

Operating income 2.21B up 878.76%

Cost of revenue 14.57B up 23.71%

Thesis Killer: No. $DIS has tailwinds as the COVID reopening continues to rollout across the world. Disney+ streaming is continuing to grow subscribers, but I didn’t like their latest announcement: Disney Plus is trying ads.

Disclosure: I am long COIN, TDOC, DDOG, SHOP.

Source: Investopedia, A Brief History of U.S. Bear Markets, October 9, 2021.

Source: https://ir.zscaler.com/#s-events